Fujikura Composites Inc. (TSE: 5121; “Fujikura Composites” or the “Company”), one of the core portfolio companies of Hibiki Path Advisors SPC (“we,” “us,” or “Hibiki”), announced its FY3/26 results and held its earnings briefing. Following our previous post, where we discussed the “offense” side of the Company’s corporate value enhancement story, we would like to turn to the “defense” side. In this second part, we will share our views on two key topics: the structural reform of the Industrial Materials business and the Company’s capital policy.

At the Annual General Meeting held on June 25, we asked the outside directors, excluding Mr. Nagahama who was absent, for their views on two points: first, whether the Company should revisit its ROE target, given that actual ROE has already exceeded the target set in the medium-term plan; and second, how they view the Company’s current Equity Ratio (Net Assets Ratio). Their response suggested to us that “the Board recognizes the need to keep discussing the right balance between financial soundness and capital efficiency in order to enhance corporate value over the medium to long term.”

We have also shared the thoughts on capital policy outlined in this post with the Company’s internal directors, and we are continuing our dialogue with them. We hope the Board will take these discussions forward and translate them into meaningful change sooner rather than later.

~~~

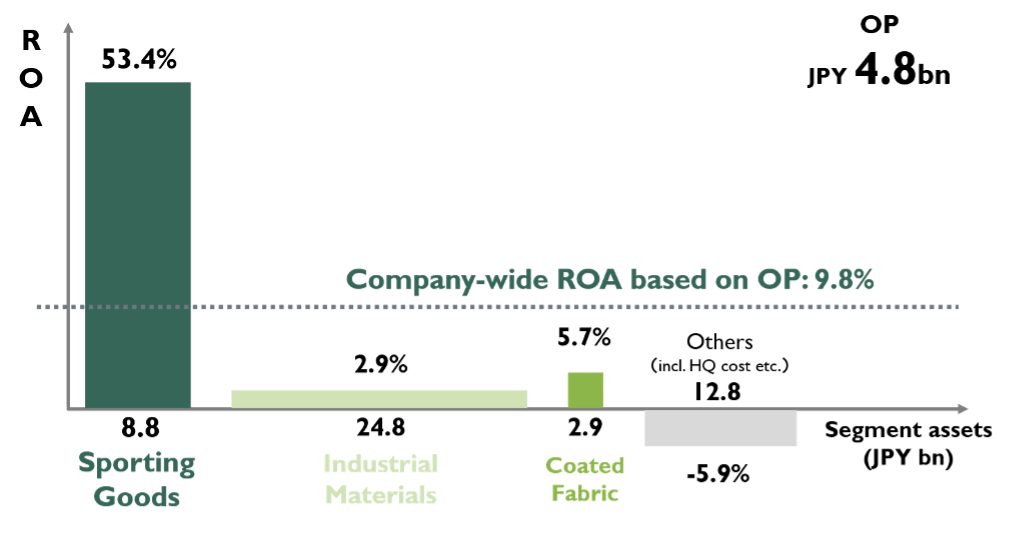

Let us start with the structural reform of the Industrial Materials business. Since sending our proposal letter last autumn, we have believed that Fujikura Composites needs to revisit how it manages its business portfolio to enhance corporate value. The Sporting Goods business has overwhelming global competitiveness and a significantly high ROA. By contrast, the Industrial Materials business has required a large allocation of assets, but has not generated a sufficient level of profit. From the perspective of improving capital efficiency across the Company, we believe this has been an area with significant room for improvement.

Figure 1: Fujikura Composites — ROA Comparison by Segment in FY3/26

* ROA: Segment profit before tax / average segment assets for FY3/25 and FY3/26

(Source: Prepared by Hibiki based on the Company’s securities reports, financial results materials, and Bloomberg)

Looking at the Company’s disclosed materials, segment operating profit (OP) margins had remained weak since peaking in 2022. Recently, however, structural reforms to improve profitability have made progress. As a result, OP in the Industrial Materials segment increased sharply to JPY 728 mn in FY3/26, up 264% year on year.

What is especially important here is that more than 90% of the increase in segment OP came from price pass-through. In a difficult business environment, particularly in automotive-related products where negotiations are never easy, the Company pushed through tough negotiations over several years and ultimately improved profit margins. We believe this deserves proper recognition.

Figure 2: Fujikura Composites — Performance and Outlook for Industrial Materials (only in Japanese)

(Source: Fujikura Composites FY3/26 Results Briefing Materials)

The Company expects profitability to continue improving significantly. For FY3/27, segment OP is forecast to increase 80% year on year to JPY 1.31 bn, while the OP margin is expected to rise from 3.1% to 5.6%. For FY3/28, the Company expects segment OP of JPY 2.5 bn, representing an increase of roughly 91% from the FY3/27 plan. Looking further ahead, the Company has set an ambitious target of at least JPY 3.4 bn in OP for FY3/31, the final year of the next medium-term plan. This implies a CAGR of 36.1% from FY3/26.

The fact that the Company has disclosed this longer-term plan suggests that the details of its structural reform plan are becoming more concrete. In May this year, the Company announced the closure of its Kasu Plant. In its cash allocation plan, the Company also clearly stated that it intends to invest approximately JPY 3 bn in restructuring the FC industrial products business, including the consolidation of production sites and investments in automation and labor-saving equipment. It also plans to invest approximately JPY 1.5 – 2.5 bn in reviewing its China operations. In addition, as growth investments, the Company plans to allocate approximately JPY 4 – 5 bn to growth areas within the Industrial Materials business, including medical, liquid detection sensors, next-generation infrastructure, next-generation mobility, and semiconductors.

This is not simply about cutting costs. The Company appears to be aiming for a more fundamental strategic reset: rebuilding the profit structure of the business while also laying the groundwork for the next stage of growth. As a shareholder, we will continue to support the Company while closely watching the steady execution of this plan.

~~~

Next, let us turn to capital policy. As we also stated in our previous post, continuing to hold up ROE of 10%, P/B of 1.0x and P/E of 10.0x as management targets, when the Company has already exceeded all three, risks sending a troubling message to the capital markets that management lacks the forward-looking ambition to enhance corporate value to the next level. The Company should revisit these targets and set a more forward-looking framework that better reflects its current earnings potential and capital position.

To begin with, the Company has, at least since FY3/17, used an Equity Ratio (Net Assets Ratio) of 60% or more as a guideline. In reality, however, it has remained well above that level for more than ten years, since FY3/14. Over the past few years in particular, ROE had been on a declining trend as profitability weakened in the Industrial Materials and Coated Fabric businesses. In our view, when profitability is under pressure, capital efficiency should receive even greater management attention. Yet the Company has continued to present an already-achieved ROE target of over 10% as a medium- to long-term target, while making no major change to its capital policy. To be candid, we see this as somewhat conservative.

Figure 3: Fujikura Composites — Net Assets Ratio Trend

(Source: Prepared by Hibiki based on the Company’s securities reports, financial results materials, and Bloomberg)

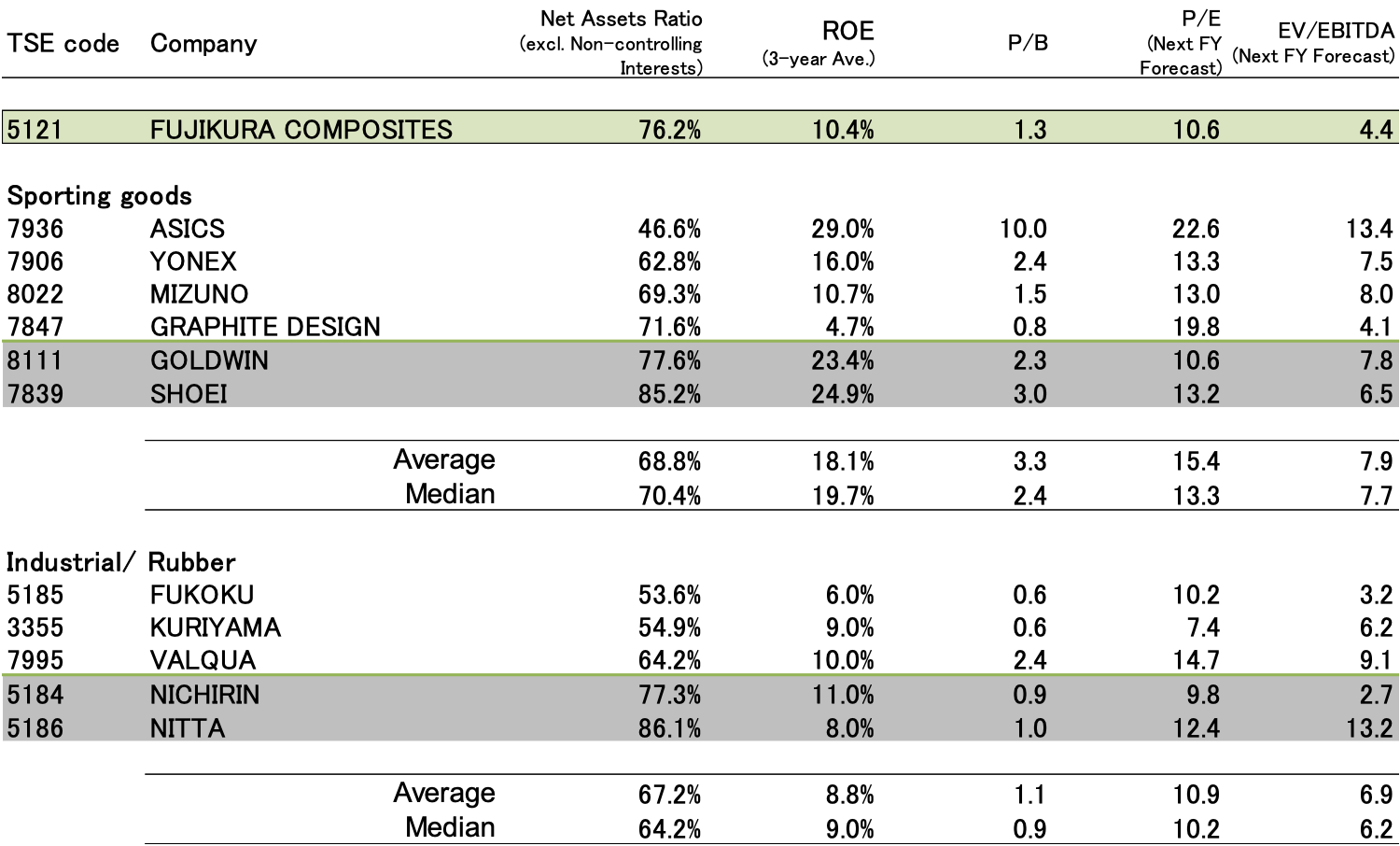

Compared with peers, Fujikura Composites’ Net Assets Ratio is high, except for certain sporting goods companies with particularly high ROE and some industrial materials companies. At the same time, the Company’s ROE does not compare favourably with Sporting Goods peers, and even against Industrial Materials peers, we would not say it is particularly high.

Figure 4: Fujikura Composites vs. Peers — Net Assets Ratio and ROE Comparison

(Source: Share prices as of the close on June 26, 2026; Bloomberg; Toyo Keizai Shikiho)

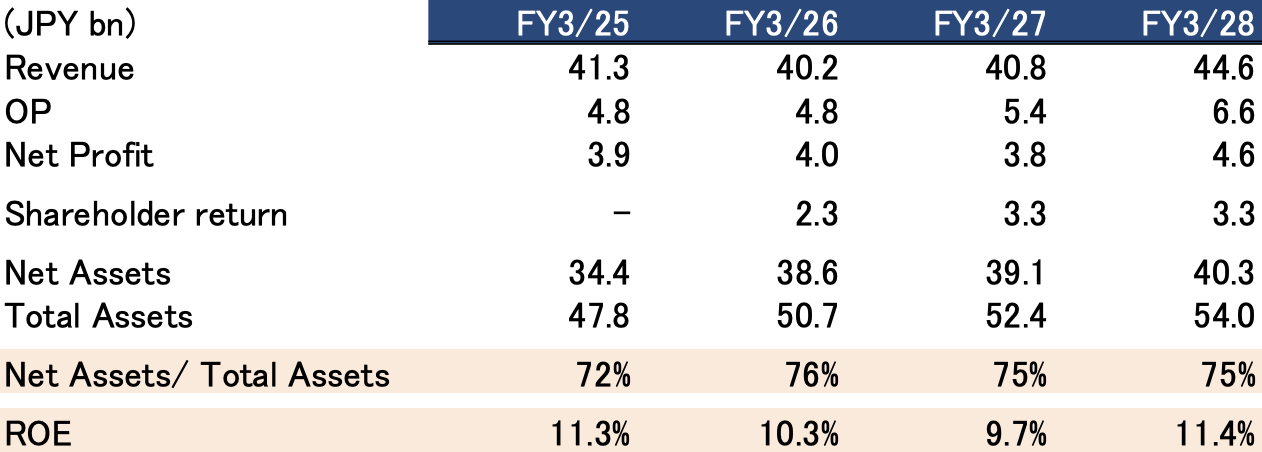

Looking ahead, our simple estimate suggests that ROE in the final year of the current medium-term plan would remain at around 11.4%, while the Net Assets Ratio would still be very high at roughly 75%. Even if structural reform in Industrial Materials progresses and the Sporting Goods business continues to grow steadily, the plan still appears to leave a large amount of equity on the balance sheet, limiting the upside to ROE. From a shareholder’s perspective, this feels like a real missed opportunity.

Figure 5: Fujikura Composites — Simple Estimate of Net Assets Ratio and ROE

* Sales and OP are based on disclosed information. Net Profit for FY3/27 is based on disclosed guidance. Net Profit for FY3/28 is estimated using the FY3/27 ratio of net profit to OP. Shareholder returns are assumed at JPY 9 bn in total; excluding amounts already executed in FY3/26, the remaining amount is allocated between FY3/27 and FY3/28. Net Assets are calculated by adding Net Profit to the prior year-end amount and subtracting shareholder returns. Total Assets are estimated on the assumption that accounts receivable and inventories move in line with sales, and that, in addition to maintenance investments broadly in line with depreciation, the Company makes active investments of approximately JPY1.5 bn in each of FY3/27 and FY3/28.

(Source: Prepared by Hibiki based on the Company’s securities reports, financial results materials, and Bloomberg)

Taking a slightly different angle, in our previous proposal we pointed out that Fujikura Ltd. may have many similarities with Fujikura Composites’ current situation. As is well known, Fujikura Ltd.’s corporate value has increased dramatically since then. Its ROE has improved significantly over the past 15 years, helping the company earn the trust of investors. On the Equity Ratio, Fujikura Ltd. has also stated in the medium-term plan announced this year that it intends to maintain a ratio of around 50%. This shows a clear stance of pursuing high ROE while maintaining a lean and resilient financial structure. We believe Fujikura Composites can learn a great deal from this more proactive approach. We hope the Company will also take a more forward-looking stance on capital policy, an area that is very much within management’s control.

Figure 6: Fujikura Ltd. (5803) — ROE Trend

* In line with Fujikura Ltd.’s disclosure, Total Assets and Net Assets excluding non-controlling interests are calculated as the average of the prior year-end and current year-end balances.

(Source: Prepared by Hibiki based on Bloomberg)

We fully recognize that Fujikura Composites has changed meaningfully over the past few years. Late last year, the Company cancelled treasury shares, and it also significantly strengthened its share-based compensation plan for directors and employees. We believe this was not just a technical change in the compensation system. It was an important step toward aligning management, employees, and shareholders around the same goal of enhancing corporate value.

That is precisely why we believe the Company now needs to raise its ambition on capital efficiency. Business restructuring and earnings improvement are important, but they should not be the end of the story. The Company also needs to make more active use of excess capital, whether through growth investments or shareholder returns. If management can show a clearer commitment to sustainably improving ROE and PBR, we believe the capital market’s view of Fujikura Composites could change meaningfully.

~~~

We hope the Company will not stop this momentum halfway. We would like to see Fujikura Composites pursue transformation across its business, financial policy, and governance, at a level and speed that exceeds the expectations of the capital market. Corporate value is maximized most quickly and most reliably when management, employees, and shareholders are all moving in the same direction. As a shareholder that supports the Company’s growth, and as a “close yet tough friend” we will continue our constructive dialogue with Fujikura Composites to help maximize its corporate value.

EOD

(Our History of Engagement)

17/June/2026 – FY3/26 Results, A Closer Look at the Growth Drivers of Its Golf Shaft Business

10/Jun/2026 – Revised Large Shareholding Report and Company Introduction Materials

2/Apr/2026 – Revised Large Shareholding Report

26/Jan/2026 – Large Shareholding Report

December 26, 2025 – Fujikura Composite’s Share Repurchase Announcement

5/Dec/2025 – Comments on Fujikura Composite 2Q Earnings Briefing

14/Nov/2025 – Submission of Our Proposal for Fujikura Composites

This post does not constitute a proposal, solicitation, marketing communication, advertisement, inducement or representation in respect of any service or product, nor does it constitute advice to buy or sell any investment product or any investment of any kind, or a recommendation to purchase or sell any investment product, make any investment, execute any transaction, or refrain from taking any other action, whether or not any terms are described. It also does not constitute an opinion regarding the merits of any particular investment or investment strategy. Any examples of strategies or transactions are provided solely for illustrative purposes and do not indicate any past or future strategy or performance, nor do they indicate the likelihood of success of any particular strategy. This post does not constitute investment, financial, legal, tax, or any other advice.

This post presents our assessments, estimates, and opinions regarding the business of FUJIKURA COMPOSITES Inc. (“FUJIKURA COMPOSITES”) and FUJIKURA COMPOSITES group companies.

This post has been prepared based on publicly available information, which we have not independently verified, and is not complete, timely, or comprehensive.

Although we believe that the information contained in this post is accurate and reliable, we make no representation or warranty as to the accuracy, completeness, or reliability of such information, or of any statements or oral communications regarding FUJIKURA COMPOSITES, FUJIKURA COMPOSITES group companies, or any other companies described herein. We also assume no responsibility for any such statements or communications, including any inaccuracies or omissions therein. With respect to public companies, there may be non-public information held by such companies or their insiders that has not been disclosed by those companies. Accordingly, all information contained in this post is presented “as is,” without any warranty of any kind, and we make no express or implied representation as to the accuracy, completeness, or timeliness of such information, or the results of its use. Readers should obtain their own professional advice and make their own assessment of the relevant matters. We disclaim any obligation or liability for any loss arising from, or in connection with, the use of all or any part of the information contained in this post, including any inaccuracies or omissions therein. Any investment involves significant risks, including the risk of a complete loss of capital. Any forecasts or estimates are provided solely for illustrative purposes and should not be regarded as indicating any upper limit of potential gains or losses. We may modify all or part of this post without notice to any person, but we are under no obligation to provide any revisions, updates, additional information or materials in relation to this post, or to correct any inaccuracies.

This post may contain content or quotations from, or hyperlinks to, publicly available third-party sources of information (“Third-Party Materials”). Permission to quote Third-Party Materials in this post may not have been sought or obtained. The contents of Third-Party Materials have not been independently verified by us and do not necessarily reflect our views. The authors and/or publishers of Third-Party Materials are independent from us and may hold views that differ from ours. The inclusion of Third-Party Materials in this post does not imply that we endorse or agree with any part of the content of such Third-Party Materials, nor does it imply that the authors or publishers of such Third-Party Materials endorse or agree with the views expressed by us in relation to the relevant matters. Third-Party Materials do not constitute all relevant news reports or views expressed by third parties regarding the matters discussed herein.

We do not intend, either by ourselves or through other shareholders, to propose at a general meeting of shareholders of FUJIKURA COMPOSITES that the business or assets of FUJIKURA COMPOSITES or FUJIKURA COMPOSITES group companies be transferred to a third party or discontinued. We also have no intention of engaging in any conduct whose purpose would be to make it difficult for FUJIKURA COMPOSITES or FUJIKURA COMPOSITES group companies to continue conducting their businesses in a stable and ongoing manner.

We currently beneficially own and/or have an economic interest in securities of FUJIKURA COMPOSITES and/or FUJIKURA COMPOSITES group companies, and may continue to beneficially own or have an economic interest in such securities in the future. With respect to our investment in FUJIKURA COMPOSITES and/or FUJIKURA COMPOSITES group companies, we may, on an ongoing basis and depending on various factors — including the financial condition and strategic direction of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, the results of discussions with FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, overall market conditions, other investment opportunities available to us, and the possibility of purchasing or selling securities of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies at prices at which we desire to transact — at any time, including through open-market or private transactions after we have established a position, buy, sell, cover, hedge, or otherwise change the form or substance of our investment, including securities of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, in any manner permitted by applicable laws and regulations, and we expressly disclaim any obligation to notify others of any such changes. We reserve the right to take any actions we deem appropriate in relation to our investment in FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies. Such actions may include, but are not limited to, communications with the board of directors, management, or other investors.