On May 11, 2026, YAGI Co., Ltd. (securities code: 7460; hereinafter the “Company” or “YAGI”), one of the core portfolio companies of Hibiki Path Advisors SPC (“Hibiki,” “we,” or “our”), announced its new medium-term management plan, Medium-Term Management Plan 2029 (Business to Belief). While continuing to derive its fundamental source of added value from the wide range of materials and fashion-trend insights accumulated through its long-standing global textile trading business, its original core business, YAGI is now decisively shifting its course toward pursuing growth on a new global stage through proactive investment as a brand-driven company. In this third installment of our five-part series introducing YAGI, we take an objective look at the down jacket market, the core product category of TATRAS, which is set to spearhead YAGI’s Brand Business.

As discussed in our previous post, TATRAS is a brand rooted in down jackets and was established in Milan in 2007 by designer Masanaka Sakao. Its name is derived from the Tatra Mountains on the border between Poland and Slovakia.¹ The three crosses in the TATRAS logo represent “elegance,” “practicality,” and “exclusivity.”² TATRAS is a distinctive brand that combines uncompromising Japanese craftsmanship with Italian aesthetics and sensuality—an understated form of elegance that wins through attention to detail rather than ostentation. The down jacket market, which TATRAS chose as its initial core category, is in fact sizeable, particularly in North America and Europe, where winter temperatures fall below freezing, and it continues to grow in Asia as income levels rise. In this post, we explain the drivers behind this market growth and introduce the key players that deserve attention.

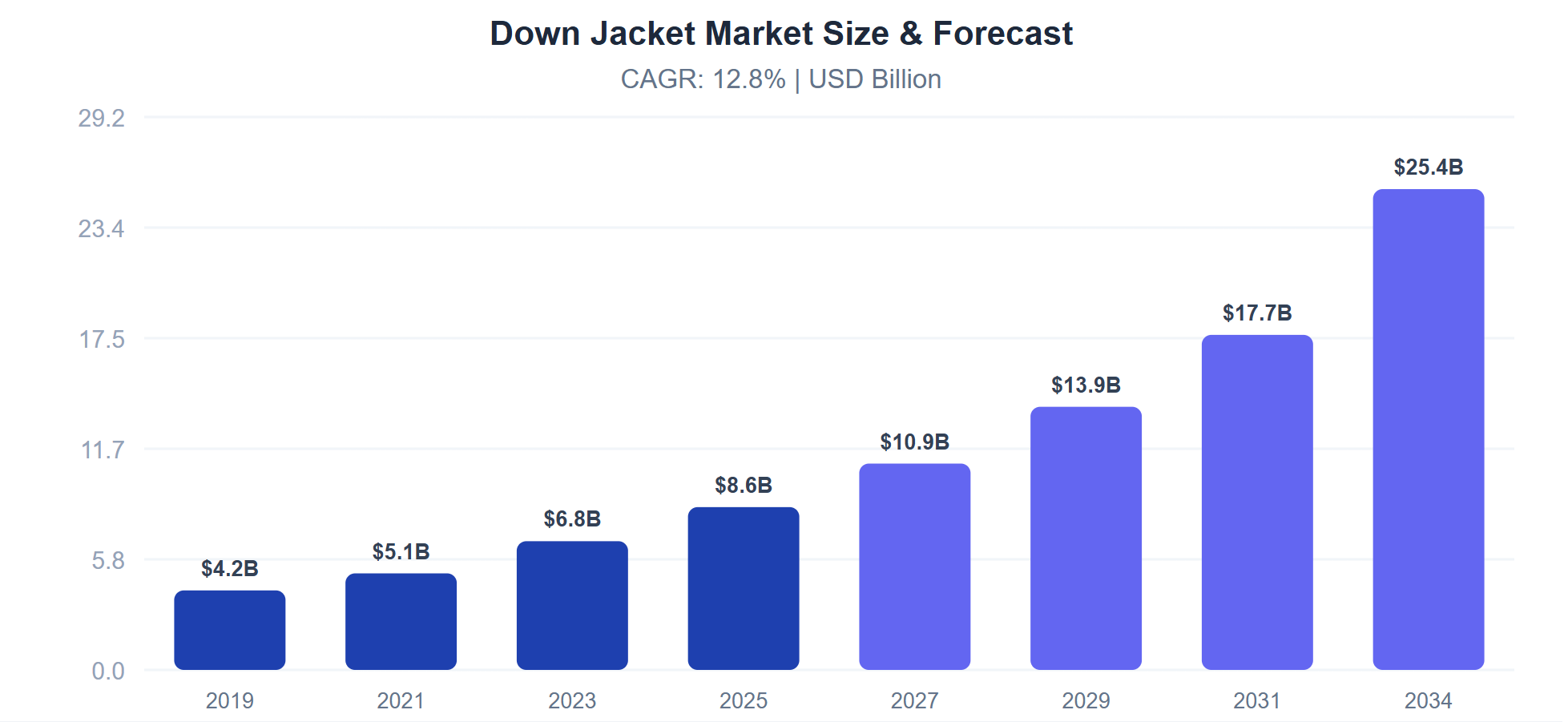

Let us begin with the size and outlook of the market. According to research by DATAINTELO, the global market is currently worth USD 8.6 billion and is projected to reach USD 26.4 billion by 2034 (see below). This represents annual growth of approximately 13%, suggesting that down jackets enjoy a distinctive growth environment even within an apparel industry that might otherwise appear mature. Why is this the case? Let’s find out.

(Source: DATAINTELO)

As one might expect, the concentration of leading down jacket brands in North America and Europe is closely linked to the severe winter climates of those regions. In sub-zero temperatures, layering lightweight garments provides limited benefit while adding bulk. The market therefore developed around the pursuit of functionality—namely, how to maximize warmth while minimizing weight. Another historically important starting point was the widespread adoption of central heating in multi-unit residential buildings, long mandated by regulation in Canada and northern U.S. cities such as Chicago and New York. In urban winters where those indoor temperatures of roughly 20C and outdoor temperatures of -10C are commonplace, the habit of simply throwing a down jacket over a T-shirt when stepping outside developed naturally.

More recently, the major catalyst that revitalized the down jacket market was the shift in lifestyles during and after the Covid-19 pandemic. As cities around the world entered lockdown and people experienced the unprecedented reality of remaining at home for extended periods, many sought respite in sparsely populated natural settings and the countryside. This gave rise to a rapid reassessment of outdoor leisure and a renewed desire to coexist with nature. It is widely recognized that the global market for hobbies such as camping and trekking expanded substantially worldwide in the wake of the pandemic; the down jacket market expanded sharply in tandem.

Finally, the recent rise of social media added further momentum. Vloggers and Instagrammers increasingly presented down jackets as stylish daily use clothing that also provide warmth in natural settings. As down jackets came to be viewed as fashion items, the luxury segment expanded rapidly as well.

The market began with warmth and functionality—light weight and water resistance—and has gained considerable depth in recent years as fashion became an increasingly important element. This distinctive market formation has also produced a diverse range of brand-development paths and origin stories. In our view, the market has the following defining characteristics:

① Many of the leading players have long corporate histories.

② Functionality and thermal performance lie at the heart of their brand stories.

③ Over the past decade, more fashion-oriented brands have entered the market.

Among the best-known winter sports and outdoor brands whose product ranges include down jackets are Patagonia, The North Face, and Columbia. Each has a history spanning more than 50 years and has built strong customer loyalty worldwide across generations as a broad outdoor brand for enjoying nature and enduring harsh winters. All three grew with an intense focus on functionality, including the performance of textiles and the quality of down used in extreme cold. Even Moncler, now virtually synonymous with premium luxury down, began in 1952 at the foot of the Alps near Grenoble as a function-led manufacturer of sleeping bags and tents designed to protect mountaineers from severe cold.

The two companies we wish to highlight in this post are Canada Goose and Moncler, both of which played major roles in transforming the down jacket from a purely functional outerwear product into a fashion item and, in the process, reshaping the market as a whole. The similarities between the two are striking: each remained anchored in an authentic brand story built on proven performance and trust in materials and sewing expertise from its founding, while elevating its fashion credentials and growing through a DTC (direct-to-consumer) strategy that enabled tighter brand control. Another intriguing commonality is that private equity funds played pivotal roles at major inflection points in both companies’ growth. As TATRAS executes its global growth strategy, we believe Canada Goose and Moncler are not only formidable incumbent competitors but also offer valuable lessons through their respective development stories.

![]() About Canada Goose (*logo used from its website)

About Canada Goose (*logo used from its website)

Canada Goose (“CG”) is now listed in both NYSE and Toronto Stock Exchange and has become a highly successful brand business with a market cap of close to USD 1 billion. Like YAGI, its story spans three generations of one family. Dani Reiss, the founder’s grandson and the current owner-CEO, partnered with Bain Capital, one of the world’s leading private equity firms, around an unwavering commitment to “Made in Canada” and the simple yet powerful mission “Free People From The Cold™.” It is a compelling example of a local outerwear factory evolving into a global premium down brand. CG traces its origins to 1957, when Polish immigrant Sam Tick established a sewing factory in Toronto and began producing wool vests, raincoats, and snowsuits. His son-in-law David Reiss joined the business in the 1970s and, following the development of a high-capacity down-filling machine, materially expanded its production capabilities for cold-weather outerwear. In the late 1970s, the company launched Snow Goose, the forerunner of Canada Goose. Yet most of its actual earnings still depended on low-margin OEM production for private-label products bearing other companies’ brand names, leaving it in a precarious hand-to-mouth position.

CG’s first major turning point came in 1997, when Dani Reiss, the founder’s grandson, joined the business. Dani had little initial interest in the family company. He earned a degree in English literature from the University of Toronto, dreamed of becoming a writer, and began working at CG part-time simply to earn some spending money. A visit to a German trade fair with his father changed his trajectory.³ Although the brand was not particularly well known in Canada, users in Germany praised it. Dani discovered that many customers in Europe and Asia cared deeply about where high-quality products were made and held Canadian-made outerwear in high regard. He abandoned his dream of becoming a writer and instead resolved to tell the story of the brand his family had protected—and of the people who wore it.

Soon thereafter, Dani proposed consolidating the company’s products under the Canada Goose name,⁴ and in 2001 he became CEO while still in his late twenties. He placed Canadian origin at the center of the brand identity. At a time when many apparel companies were shifting production to Asia, he eliminated any avenue of retreat by declaring that Canada Goose would remain 100% made in Canada. He also maintained strict pricing discipline without relying on discounts and implemented a strategy that transformed the production process itself—how each product was made—into brand value. The brand gained global recognition after making its screen debut in two 2004 films, The Day After Tomorrow and National Treasure, and steadily built a track record as “the down jacket genuinely trusted in extreme cold.”⁵

The decisive inflection point that propelled CG onto a much steeper growth trajectory came in 2013, when it received growth capital from Bain Capital. Bain and Dani Reiss (including his asset-management company) came to jointly own the business with a 70/30 split. Bain is said to have prevailed over competing bids because it committed to: (1) retaining Dani as CEO; (2) respecting the Company’s commitment to Made in Canada; (3) providing strategic and operational support for overseas expansion and the shift to DTC; and (4) funding the expansion of domestic manufacturing capacity. The design philosophy was clear: preserve the corporate identity while drawing on external expertise to strengthen execution capabilities in DTC, supply chain management, IT, international sales, and other areas. This is in fact similar to TATRAS joining the YAGI Group in 2014 to pursue its next phase of growth, although the speed and global execution capabilities of private equity investors are, candidly, remarkable.

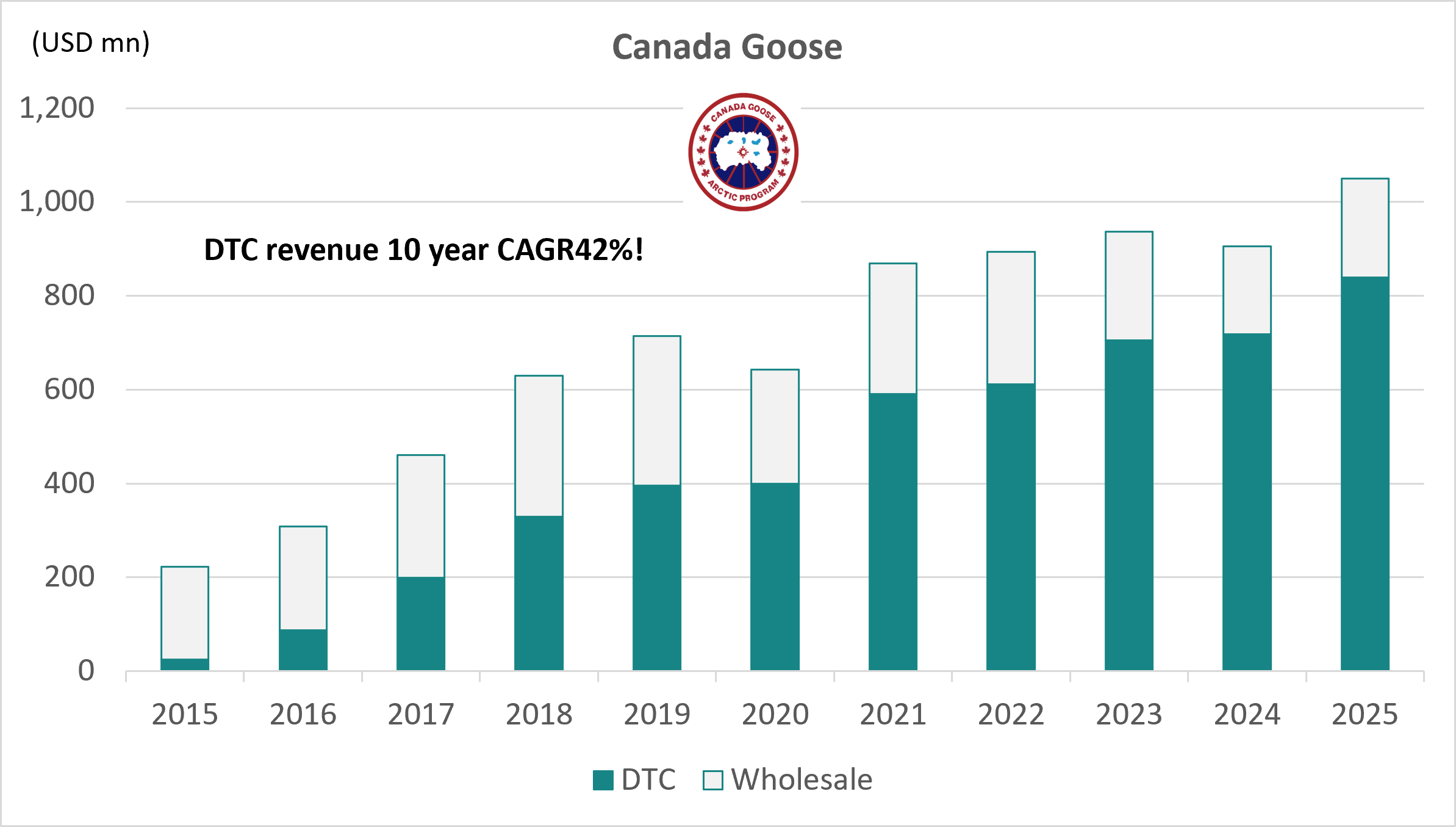

In 2014, CG launched e-commerce in Canada and subsequently expanded it into the United States, Europe, and Asia. It opened its first flagship stores in Toronto and New York in 2016, followed by Tokyo in 2017 and Beijing and Hong Kong in 2018, accelerating both its O2O (online-to-offline) and DTC strategies in parallel. The company listed in 2017 to facilitate a partial exit by Bain. As shown below, however, it has continued to grow under Dani’s leadership, with DTC still accounting for more than 80% of sales. While maintaining control over brand power and pricing, it has also been gradually expanding into spring and summer products to reduce excessive dependence on winter merchandise.

Although its corporate history is not nearly as long as YAGI’s, CG also places great importance on its heritage (see here).

Canada Goose Revenue by Segment

* Excludes the “Other” segment.

(Source: Hibiki Path Advisors SPC compiled from Canada Goose public disclosures and Bloomberg)

![]() About Moncler (*logo used from its website)

About Moncler (*logo used from its website)

Founded in 1952 as a small mountain-equipment manufacturer near Grenoble, France, Moncler initially operated on a modest scale, producing practical products for people working in extreme cold, including sleeping bags, tents, and padded work coats. Its profile rose sharply after it supplied apparel to the French ski team at the Winter Olympics, and its following expanded during the 1980s. However, its positioning between fashion and functionality became ambiguous. It struggled to compete with luxury houses such as Prada and Gucci and sports brands such as The North Face, entering a prolonged period of stagnation and repeated changes of ownership.

The major turning point was when Remo Ruffini bought Moncler in 2003. Born into a family of textile entrepreneurs, Ruffini—who remains Moncler’s chairman today—had already achieved success in the apparel industry by founding and subsequently selling a men’s shirt brand. He understood Moncler’s “dormant brand value” better than anyone. Immediately after the acquisition, he introduced the concept of “piumino globale”: a vision of making the down jacket the centerpiece of every setting—from mountains to cities, from sport to everyday life, and from winter-sports enthusiasts to urban consumers around the world.⁶ We understand this as a strategy that first concentrated resources on the down category, while deliberately broadening both occasions of use and customer segments to achieve “luxury × universality.” Just as Canada Goose established a simple, powerful core around “Made in Canada” and “Free People From The Cold™,” Moncler recentered its story on its origins as “the only luxury brand with roots in the mountains,” reinterpreting its heritage in polar expedition gear through the lens of urban luxury.

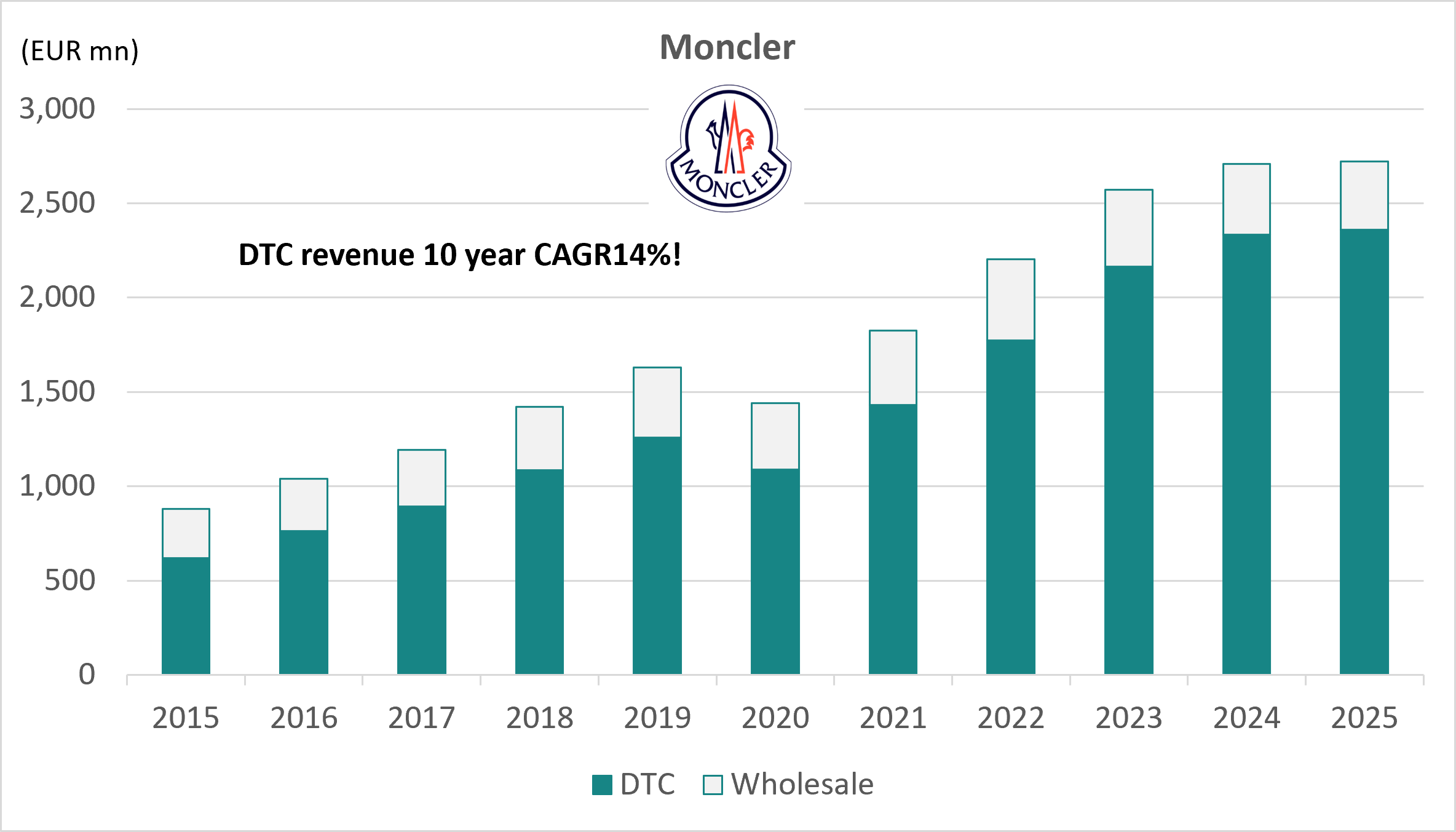

Under Ruffini, Moncler effectively created the high-end luxury market for down jackets and has remained its defining company. After repositioning the brand into a higher price tier, it focused on DTC—directly operated stores and proprietary e-commerce—from the outset in order to exercise complete control over supply and brand messaging. Its success story reflects an exceptionally deep strategy that communicates both its functional French and Alpine roots and Italian style and tailoring. Its luxury-focused insistence on premium pricing and disciplined supply closely resembles Canada Goose’s refusal to depend on discounting while protecting Made in Canada. As a result, Moncler had expanded to 295 directly operated stores as of FY2025.

Moncler Revenue by Segment

* Moncler brand only.

(Source: Hibiki Path Advisors SPC compiled from Bloomberg)

Moncler’s approach to cultivating brand culture is also distinctive. Through initiatives such as “Moncler Genius,”⁷ which brings together multiple designers and brands, and “The Art of Genius,”⁸ which convenes “geniuses” from music, street culture, automobiles, art, and other fields, Moncler has positioned itself not simply as a maker of cold-weather clothing, but as a platform embodying abstract values such as challenge, diversity, and creativity. Whereas Canada Goose cultivated authenticity in environments that confront the cold—from film shoots in frigid locations to nightclub bouncers—Moncler has strengthened its position as a luxury brand by creating a forum where creative talent intersects.

Another indispensable element of the Moncler story is its capital strategy: the company has grown by continually changing partners to match each stage of its development. In the first private-equity stage, Mittel and Progressio, which Ruffini brought in soon after his acquisition, acted as restructuring partners, supporting the repair of the balance sheet and the rationalization of licensing arrangements. Importantly, just as Bain retained Dani as CEO when it invested in Canada Goose, the two funds kept Ruffini at the helm. They also seconded executives to support him, including a veteran of Ralph Lauren and the architect of Calvin Klein’s restructuring plan. Carlyle, which took the baton as the next partner in 2008, expressed unequivocal confidence in Ruffini in its investment announcement, describing Moncler as “a historic sport-luxury brand” that had regained “an important and authoritative role in the market.”⁹ Carlyle supported the company while limiting its operational involvement largely to governance.

In the second private-equity stage, Carlyle served as the growth-phase partner responsible for accelerating global DTC and elevating Moncler into a top luxury brand. It rapidly expanded the global store network, including in Asia and the United States, where Moncler had no stores before Carlyle’s investment, increasing the number of directly operated stores from six to 135 within several years. Moncler launched e-commerce in 2011. Carlyle also pursued portfolio reforms designed to establish Moncler as a luxury brand, including the disposal of non-core sports brands. From 2008 to 2012, revenue increased by 206% and EBITDA by 311%.¹⁰

In the third private-equity stage, Eurazeo, a French private equity firm that we infer was introduced by Carlyle, took the baton in 2011 to put the finishing touches on Moncler’s establishment as a global luxury down-jacket brand. Eurazeo added a stronger luxury dimension to the DTC strategy built by Carlyle. It created “luxurious living spaces” in stores located primarily in cities closely associated with fashion and luxury—including Paris, Tokyo, London, and Milan—and completed the transformation of Moncler’s luxury credentials through a bolder product lineup and a more refined brand experience.¹¹ Moncler listed its shares in Mercato Telematico Azionario, now Borsa Italiana, in 2013 and has since grown into a major group with a market cap of approx. EUR 15 billion.

Just as Canada Goose achieved explosive growth in DTC and global expansion by partnering with Bain Capital, Moncler’s growth trajectory steepened sharply around Carlyle’s investment. It subsequently continued to improve both scale and quality by assigning distinct roles at each stage to first-class partners including Eurazeo, Temasek, and LVMH. The shared principle is this: both companies have steadfastly protected their core—their roots, stories, and brand cultures—while using the capabilities of external partners to develop, to the fullest possible extent, the infrastructure required to bring that core to the world, including supply capacity, DTC, IT, and international sales.

~~~~

We have introduced two companies that have led the transformation and growth of today’s down jacket market. TATRAS remains a challenger in terms of scale, but the “rules of engagement” in the luxury market that these two companies effectively created offer many useful lessons. We believe TATRAS can analyze those lessons and build its own distinctive growth strategy upon them. Remarkably, both CG and Moncler: (1) began with products of inherently high quality; (2) preserved owner-led leadership and a strong commitment to the brand; (3) avoided indiscriminately expanding across numerous brands and instead pursued a focused strategy of maximizing the value of the original brand; and (4) at critical moments, made effective use of private equity expertise and capital to accelerate growth.

With YAGI—who possess deep expertise in textile materials and distribution—as its parent company, Milan-born TATRAS has steadily enhanced its quality and recognition while expanding brand value. Its next phase of growth should be exciting to watch. In a fashion market where the global penetration of social media has strengthened network effects, the range of potential paths to success is also becoming more diverse. In our next post, we will discuss what we see as “TATRAS’s path to winning.” Please stay tuned!

¹ TATRAS Launches Its Spring/Summer 2021 Campaign Visuals | WEAVA Co., Ltd. press release

² Rakuten Ichiba: Search by Brand – BRAND > T > TATRAS | MSS

³ The CEO of Canada Goose on Creating a Homegrown Luxury Brand

⁴ The History Of Canada Goose

⁵ Our History | Canada Goose | Canada Goose CA

⁶ Torrisi_Salvatore_Antonino.pdf

⁷ 4-MONCLER-SIMONE-ROCHA-PRESS-RELEASE_ENG.pdf

⁸ Microsoft Word – THE ART OF GENIUS POST EVENT PRESS RELEASE_ENG.docx

⁹ The Carlyle Group To Acquire A 48% Stake In Moncler Group | Carlyle

¹⁰ moncler_case_study_0.pdf

¹¹ MONCLER: METAMORPHOSIS OF A LUXURY ICON – EURAZEO STORIE –

This post does not constitute a proposal, solicitation, marketing communication, advertisement, inducement or representation in respect of any service or product, nor does it constitute advice to buy or sell any investment product or any investment of any kind, or a recommendation to purchase or sell any investment product, make any investment, execute any transaction, or refrain from taking any other action, whether or not any terms are described. It also does not constitute an opinion regarding the merits of any particular investment or investment strategy. Any examples of strategies or transactions are provided solely for illustrative purposes and do not indicate any past or future strategy or performance, nor do they indicate the likelihood of success of any particular strategy. This post does not constitute investment, financial, legal, tax, or any other advice.

This post presents our assessments, estimates, and opinions regarding the business of Yagi & Co., Ltd. (“Yagi”) and Yagi group companies.

This post has been prepared based on publicly available information, which we have not independently verified, and is not complete, timely, or comprehensive.

Although we believe that the information contained in this post is accurate and reliable, we make no representation or warranty as to the accuracy, completeness, or reliability of such information, or of any statements or oral communications regarding Yagi, Yagi group companies, or any other companies described herein. We also assume no responsibility for any such statements or communications, including any inaccuracies or omissions therein. With respect to public companies, there may be non-public information held by such companies or their insiders that has not been disclosed by those companies. Accordingly, all information contained in this post is presented “as is,” without any warranty of any kind, and we make no express or implied representation as to the accuracy, completeness, or timeliness of such information, or the results of its use. Readers should obtain their own professional advice and make their own assessment of the relevant matters. We disclaim no obligation or liability for any loss arising from, or in connection with, the use of all or any part of the information contained in this post, including any inaccuracies or omissions therein. Any investment involves significant risks, including the risk of a complete loss of capital. Any forecasts or estimates are provided solely for illustrative purposes and should not be regarded as indicating any upper limit of potential gains or losses. We may modify all or part of this post without notice to any person, but we are under no obligation to provide any revisions, updates, additional information or materials in relation to this post, or to correct any inaccuracies.

This post may contain content or quotations from, or hyperlinks to, publicly available third-party sources of information (“Third-Party Materials”). Permission to quote Third-Party Materials in this post may not have been sought or obtained. The contents of Third-Party Materials have not been independently verified by us and do not necessarily reflect our views. The authors and/or publishers of Third-Party Materials are independent from us and may hold views that differ from ours. The inclusion of Third-Party Materials in this post does not imply that we endorse or agree with any part of the content of such Third-Party Materials, nor does it imply that the authors or publishers of such Third-Party Materials endorse or agree with the views expressed by us in relation to the relevant matters. Third-Party Materials do not constitute all relevant news reports or views expressed by third parties regarding the matters discussed herein.

We do not intend, either by ourselves or through other shareholders, to propose at a general meeting of shareholders of Yagi that the business or assets of Yagi or Yagi group companies be transferred to a third party or discontinued. We also have no intention of engaging in any conduct whose purpose would be to make it difficult for Yagi or Yagi group companies to continue conducting their businesses in a stable and ongoing manner.

We currently beneficially own and/or have an economic interest in securities of Yagi and/or Yagi group companies, and may continue to beneficially own or have an economic interest in such securities in the future. With respect to our investment in Yagi and/or Yagi group companies, we may, on an ongoing basis and depending on various factors — including the financial condition and strategic direction of Yagi and Yagi group companies, the results of discussions with Yagi and Yagi group companies, overall market conditions, other investment opportunities available to us, and the possibility of purchasing or selling securities of Yagi and Yagi group companies at prices at which we desire to transact — at any time, including through open-market or private transactions after we have established a position, buy, sell, cover, hedge, or otherwise change the form or substance of our investment, including securities of Yagi and Yagi group companies, in any manner permitted by applicable laws and regulations, and we expressly disclaim any obligation to notify others of any such changes. We reserve the right to take any actions we deem appropriate in relation to our investment in Yagi and Yagi group companies. Such actions may include, but are not limited to, communications with the board of directors, management, or other investors.