Fujikura Composites Inc. (TSE: 5121; “Fujikura Composites” or the “Company”), one of the core portfolio companies of Hibiki Path Advisors SPC (“we,” “us,” or “Hibiki”), announced its FY3/26 results on May 11, 2026, and held its earnings briefing on June 12. At the briefing (only in Japanese), the Company reaffirmed its plan to deliver consecutive record operating profits (“OP”) in FY3/27 and FY3/28, the final year of its current medium-term management plan. It also laid out: (i) a detailed and concrete growth strategy for the Sporting Goods business; and (ii) a clear direction for the restructuring of the Industrial Goods business. We also had the opportunity to hear directly from Mr. Wakabayashi, General Manager of the ACP Business Division and head of the golf shaft business. His presentation and answers carried particular weight because they came from the executive leading the business on the ground.

In autumn 2025, we made four public proposals to the Company: (1) a fundamental overhaul of its IR activities; (2) the adoption of a 17% ROE target and stronger shareholder returns to bring the equity ratio down to 60%; (3) expanded equity-based compensation for internal directors and employees; and (4) the introduction of disciplined business portfolio management. We see the latest disclosures as a meaningful step forward on (1) IR and (4) business portfolio management.

On the other hand, we were deeply disappointed to see no revision to the Company’s ROE target. Continuing to hold up ROE of 10%, P/B of 1.0x and P/E of 10.0x as management targets, when the Company has already exceeded all three, risks sending a troubling message to the capital markets that management lacks the forward-looking ambition to enhance corporate value to the next level. In our view, these targets need to be revisited urgently. We look forward to further disclosures from the Company by the time of its first-half results briefing and will continue to engage constructively in the meantime.

We would now like to share the key points that stood out to us in the latest earnings results. The disclosures offered meaningful insights into both the “offense” and “defense” of the Company’s corporate value enhancement strategy, so we will cover them in two separate posts. In this first part, focused on “offense,” we look at the overall results and unpack the growth story of the Sporting Goods business, the Company’s main earnings driver. In the second part, focused on “defense,” we will discuss the restructuring of the Industrial Goods business, where there is significant scope for earnings improvement, as well as the Company’s capital policy.

We have also prepared our easy-to-digest introduction of Fujikura Composites, which we invite interested readers to take a look at separately.

~~~

Starting with the overall FY3/26 results (only in Japanese), revenue came in at JPY40.2 bn, down 0.9% year on year, while OP rose 4.7% to JPY4.8 bn. This was a high-quality set of results: the Company grew profits even as revenue declined. The operating margin improved from 11.3% to 12.0%, showing that Fujikura Composites is not simply defending its top line but steadily strengthening the underlying profit structure. We see this as a solid set of results that laid a firmer foundation for future growth. OP based ROA also remained close to 10%. At the same time, the equity ratio remains exceptionally high at 76.2%, once again highlighting just how much room there is to improve ROE by introducing greater capital discipline.

The segment results were equally telling. OP in the Industrial Goods business jumped from JPY200 mn to JPY730 mn, up 264% year on year. For FY3/27, the Company is targeting OP of JPY1.3 bn, up a further 80%, supported by a sharp improvement in the semiconductor manufacturing equipment market. The Coated Fabrics business also returned to the black, posting OP of JPY165 mn after an operating loss of JPY132 mn in the previous year. Meanwhile, the Sporting Goods business remained the Company’s overwhelmingly dominant earnings engine, generating OP of JPY4.7 bn. Taken as a whole, the picture is clear: Fujikura Composites is preserving the outstanding profitability of its Sporting Goods business while steadily lifting the earnings base across the rest of the portfolio. What particularly impressed us was that the Sporting Goods business maintained its OP despite the absence of a new product launch in the United States. This highlights the strength of its brand, pricing power and sales capabilities, and shows that the business does not depend on a constant stream of new product launches. We also see further upside from the new VENTUS product launched at the end of January this year. The U.S. subsidiary’s January-March 2026 results will begin to be reflected in the consolidated result from the 1Q of FY3/27.

For FY3/27, the Company is guiding for revenue of JPY40.8 bn, up 1.4% year on year, and OP of JPY5.4 bn, up 11.6%. The OP margin is expected to improve further, from 12.0% in FY3/26 to 13.2%, its highest level in 15 years. This is not simply a volume-growth story. We believe it is a sign that several years of steady work on pricing, product mix, production efficiency and the scaling back of structurally unprofitable operations are finally beginning to come through meaningfully in the numbers.

~~~

We now turn to the newly disclosed growth strategy for the golf shaft business. The first thing we want to say is that the depth and quality of disclosure this time were on an entirely different level. We have consistently made proposals aimed at enhancing the corporate value, and one principle has always been at the heart of those proposals: Company should provide proper information about its business for investors and shareholders for them to understand how much it may worth. At this briefing, the Company provided far richer information than ever before on the golf shaft business’s competitive advantages, market environment and growth strategy. We are fond of the management and IR team for taking disclosure this far. Three points in the new materials stood out to us in particular.

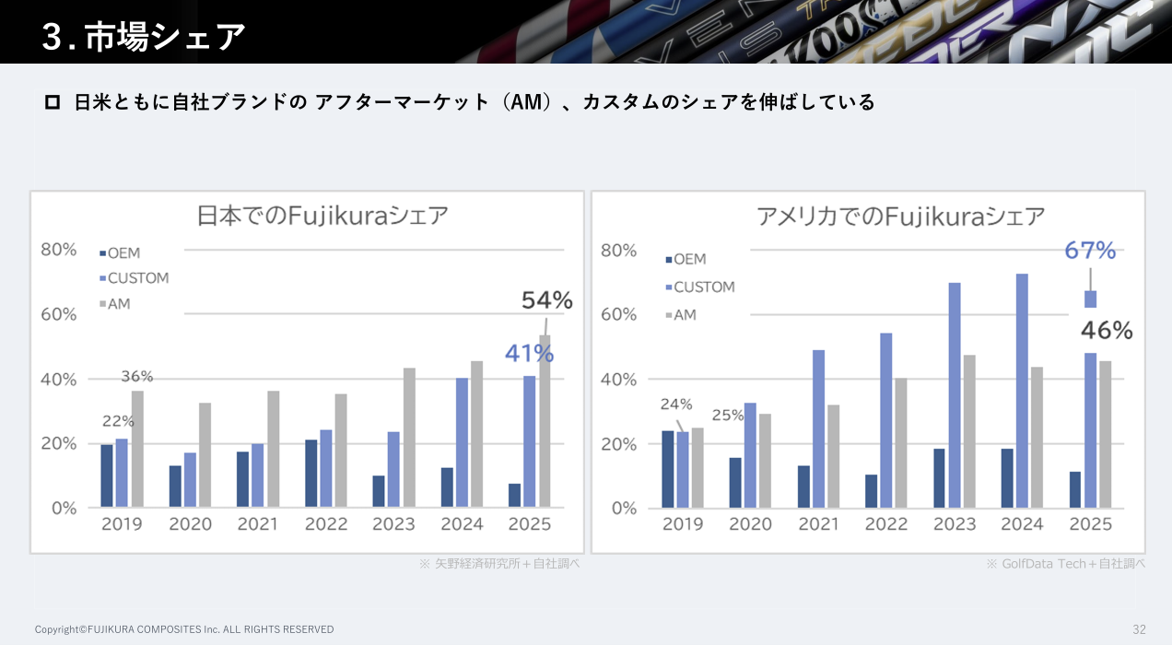

The first is that the Company holds dominant market shares in the highly profitable CUSTOM and After markets in Japan and the United States, while the contribution from lower-margin OEM operations continues to decline. In other words, the product mix within the Sporting Goods business is moving steadily in the right direction.

Figure 1: Market Share of Fujikura Composites’ Golf Shaft Business (only in Japanese)

(Source: Fujikura Composites FY3/26 Earnings Presentation)

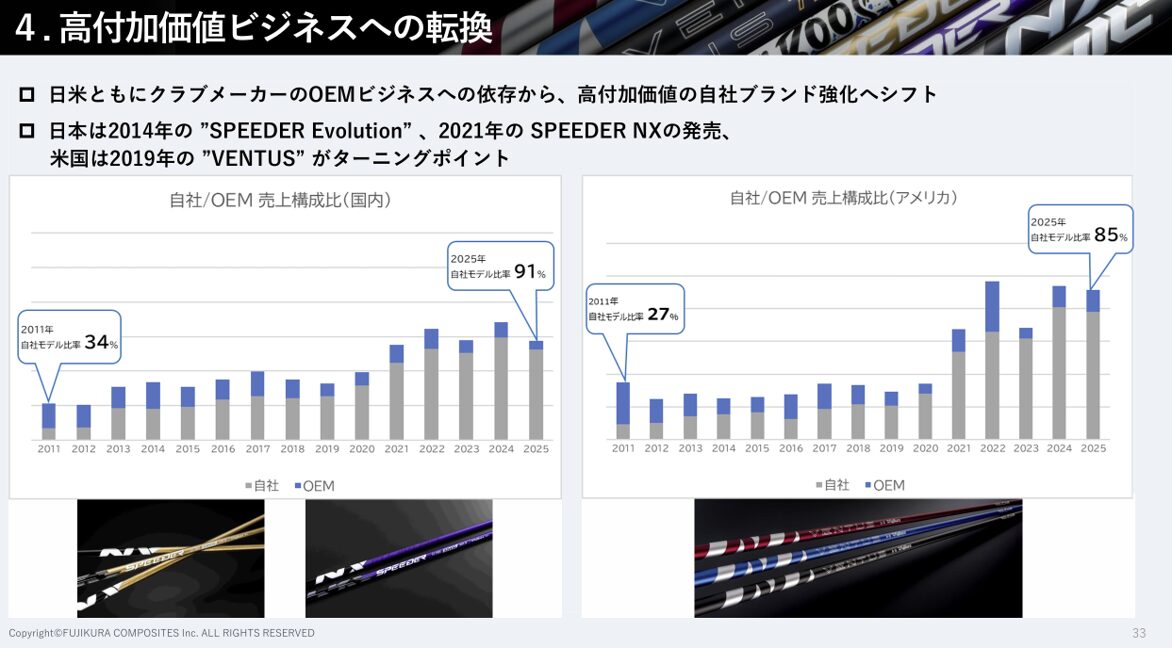

What came through particularly clearly at the briefing was that Fujikura Composites is no longer simply a shaft manufacturer. It is becoming a true brand owner. The Company has now largely moved away from the traditional OEM model, with proprietary brands accounting for an exceptionally high share of sales in both Japan and the United States. In our view, the transformation of its business model is already essentially complete.

Figure 2: Proprietary Brand Ratio of Fujikura Composites’ Golf Shaft Business (only in Japanese)

(Source: Fujikura Composites FY3/26 Earnings Presentation)

We see several major advantages to building a strong proprietary brand.

・First, it gives the Company a direct customer touchpoint through its own brand. In an OEM business, customer recognition, loyalty and insights tend to accumulate with the brand owner. With a proprietary brand, these valuable assets accrue directly to Fujikura Composites. Brands are not built overnight. They are the product of years of trust, performance and consistency. Fujikura Composites has earned strong support from the world’s leading players and serious golfers alike, and this brand equity has become a formidable barrier to entry in its own right.

・Second, it creates real pricing power. Businesses today face rising costs across raw materials, logistics, labor and much more. In an OEM-led model, price negotiations tend to revolve around manufacturing costs, with customers constantly pushing suppliers to bring those costs down. A company with its own brand, by contrast, can price according to the value it delivers through technology, performance and the strength of the brand itself. We were pleased to see “pricing optimization” repeatedly emphasized in the Company’s restructuring plans. In fact, the Sporting Goods business is already a textbook example of what that strategy should look like: use superior technology and brand strength to set the right price and earn attractive margins. This is more than just a successful business. It is a valuable management playbook that should be applied across the rest of the portfolio.

・Third, it brings the Company closer to its customers. Having a world-leading market position while receiving feedback directly from end users is an incredibly powerful combination to even strengthen its leading edge further in this data driven world. The ability to feed product reviews and requests for improvement quickly back into development creates a virtuous cycle that reinforces the Company’s competitive advantage. We believe this customer-driven development model is one of the main reasons Fujikura Composites has remained at the forefront of the market for so long.

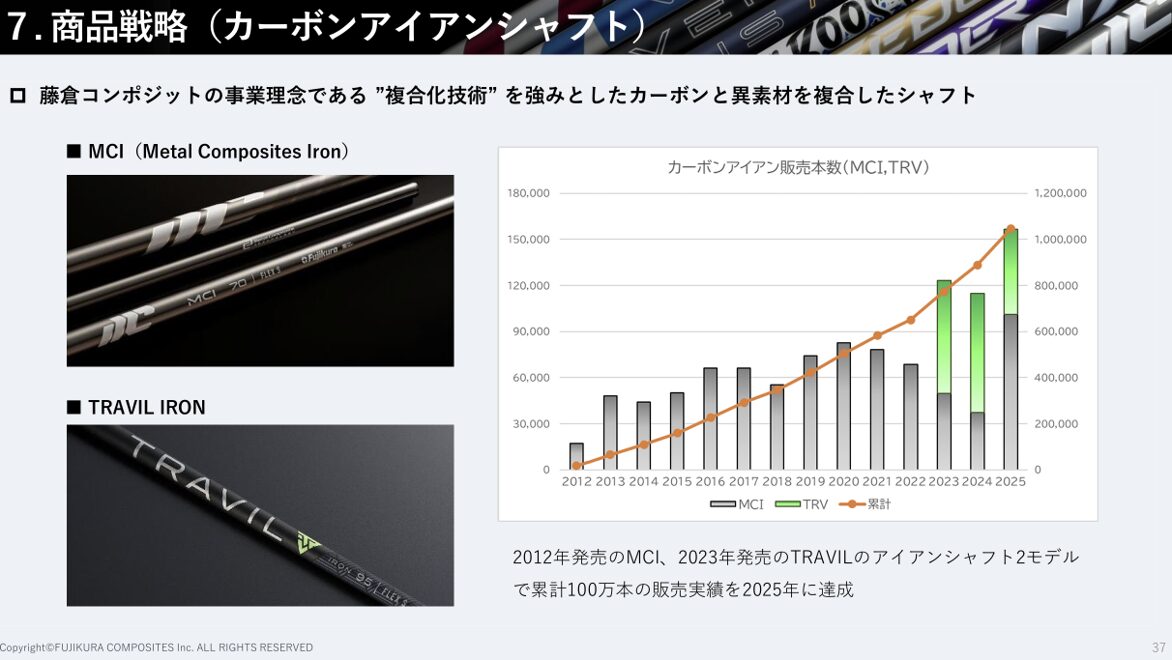

The second point is that the path to future growth is looking much more concrete. At the briefing, the Company identified two key growth drivers: (i) expanding in the iron shaft market; and (ii) stepping up sales in Europe. Steel shafts still dominate the iron shaft market, but the share of carbon based iron shafts in the aftermarket reportedly rose from 20% in 2022 to around 26% in 2025. A structural shift is already underway. Benefiting from this trend, carbon iron shafts have reportedly grown to account for 20% of the Company’s golf shaft sales. According to several market research reports, the iron shaft market, including the aftermarket, is the largest segment of the overall golf shaft market, accounting for approximately 40% to 45%¹. That makes it larger than the driver and fairway wood shaft market, which accounts for roughly 35%¹ and has historically been Fujikura Composites’ core battleground. As the advantages of carbon shafts, including lower weight, greater distance and easier swingability, become more widely understood, the market could undergo a fundamental structural shift. As the leading carbon shaft brand, Fujikura Composites could be the biggest beneficiary. The new disclosures make it clear that the Company’s carbon iron shaft strategy, centered on MCI, TRAVIL, and AXIOM, is a genuinely exciting equity story.

Figure 3: Sales Growth of Fujikura Composites’ Carbon Shafts (only in Japanese)

(Source: Fujikura Composites FY3/26 Earnings Presentation)

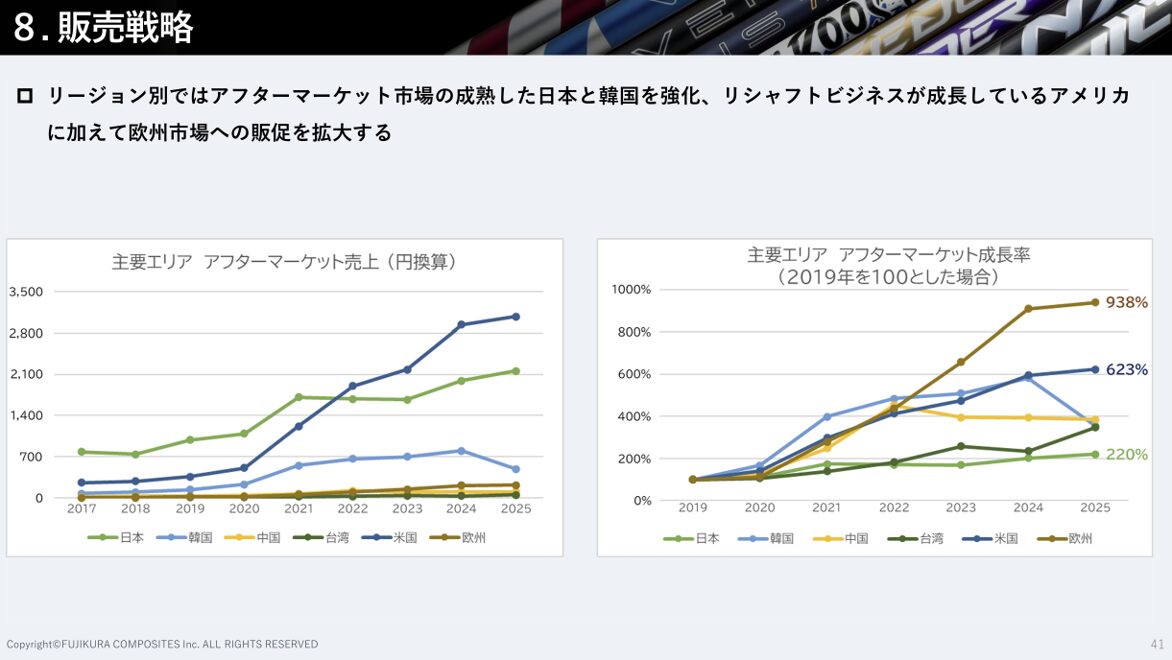

Europe is another compelling opportunity. The Company’s highly profitable aftermarket business is currently concentrated in Japan and the United States, but the new disclosure materials suggest that Europe may be even more attractive from a growth perspective. Compared with 2019, the U.S. market has expanded approximately 6.2 times, already an impressive rate of growth, while the European market has grown approximately 9.4 times. Fujikura Composites has already built overwhelming brand strength in Japan and the United States. By now making a serious push into this fast-growing market, the Company is in an excellent position to capture the full extent of that market growth.

Based on several market research reports, Europe is estimated to account for approximately 28% to 30% of the global golf shaft market¹. It is the world’s second-largest market after North America, which represents approximately 35% to 40%, meaning that Europe is roughly 70% to 80% the size of North America. Fujikura Composites’ golf shaft business still appears heavily weighted toward North America. If the Company can build greater brand awareness and a broader distribution network in Europe, where it has recently stepped up its efforts, the region could become a major driver of medium- to long-term revenue growth.

Figure 4: Aftermarket Size and Growth by Region (only in Japanese)

(Source: Fujikura Composites FY3/26 Earnings Presentation)

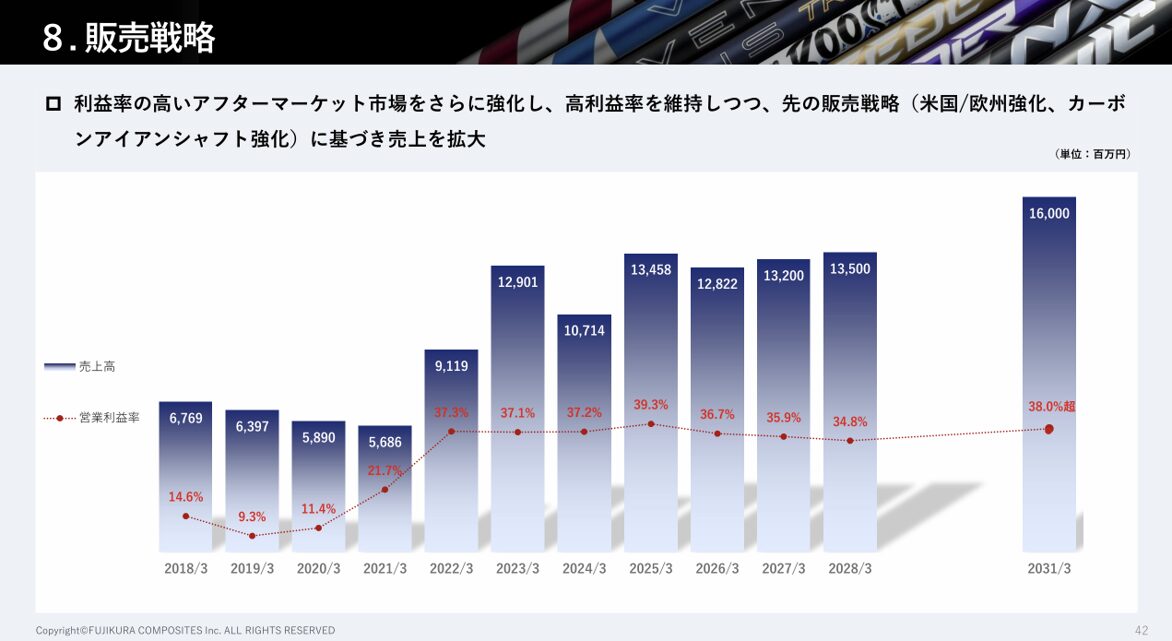

Finally, the Company unveiled ambitious FY3/31 targets for the Sporting Goods business, corresponding to the final year of its next medium-term management plan: revenue of JPY16.0 bn and an OP margin of more than 38%. This implies segment profit of approximately JPY6.1 bn, up from JPY4.7 bn in FY3/26, or roughly 1.3 times over five years. The targets appear to assume a period of limited growth during the current medium-term plan, followed by annual profit growth of around 10% over the next three years. During the Q&A session, management also explained that the plan had been drawn up on the assumption that weakness in the global golf market would continue. Since then, however, both the business environment and new product sales have reportedly been running ahead of the assumptions used when the plan was prepared, according to the management. Sales of the new VENTUS product in the United States have been particularly solid. While management noted that it is still too early to discuss revising the forecast, it appears that conditions have improved since those targets were set.

Figure 5: Long-Term Targets for Fujikura Composites’ Sporting Goods Business (only in Japanese)

(Source: Fujikura Composites FY3/26 Earnings Presentation)

We believe that these new disclosures would provide investors more circumstantial evidences to be excited about the growth prospects of the Sporting Goods segment, the Company’s core earnings pillar. We hope the readers to feel the same. In our next post, we will turn to the “defense” side of the story and discuss the restructuring of the Industrial Goods business and the Company’s capital policy.

Finally, we are genuinely encouraged to see Fujikura Composites driving meaningful change in both its operations and its approach to IR. But better earnings and clearer disclosure must never become an excuse to push capital policy down the priority list. There can be no compromise on this point. Corporate value enhancement journey requires progress on every relevant front, delivered at both the level and the speed expected by the capital markets. A higher market valuation would benefit far more than shareholders alone. Those benefits would ultimately flow through to management and employees, supporting their well-being and creating a brighter future for everyone involved. That should be the ideal essence of what capitalism actually are meant to be.

We firmly believe that corporate value appreciates the fastest when management, employees and shareholders are aligned around the same goal. We hope this new approach to disclosure marks the beginning of that alignment and look forward to seeing it translate into sustained corporate value creation.

EOD

¹ Market Growth Reports, Golf Shaft Market Report (2025) — iron shafts ~40%, steel ~55% within irons, Global Market Insights (GMI), Golf Shaft Market Analysis — iron shafts ~40% share (2022), Intel Market Research, Golf Shaft Market Outlook — iron shafts >40%, Credence Research, Golf Shaft Market Report — Europe ~28%, Cognitive Market Research, Golf Shaft In-Depth Market Report — Europe accounts for ~30%+ of global revenue share (2024)

(Our History of Engagement)

10/Jun/2026 ー Fujikura Composites: Revised Large Shareholding Report and Company Introduction Materials

2/Apr/2026 Fujikura Composites: Revised Large Shareholding Report

26/Jan/2026 – Fujikura Composites: Large Shareholding Report

December 26, 2025 – Fujikura Composite’s Share Repurchase Announcement

5/Dec/2025 – Comments on Fujikura Composite 2Q Earnings Briefing

14/Nov/2025 – Submission of Our Proposal for Fujikura Composites

This post does not constitute a proposal, solicitation, marketing communication, advertisement, inducement or representation in respect of any service or product, nor does it constitute advice to buy or sell any investment product or any investment of any kind, or a recommendation to purchase or sell any investment product, make any investment, execute any transaction, or refrain from taking any other action, whether or not any terms are described. It also does not constitute an opinion regarding the merits of any particular investment or investment strategy. Any examples of strategies or transactions are provided solely for illustrative purposes and do not indicate any past or future strategy or performance, nor do they indicate the likelihood of success of any particular strategy. This post does not constitute investment, financial, legal, tax, or any other advice.

This post presents our assessments, estimates, and opinions regarding the business of FUJIKURA COMPOSITES Inc. (“FUJIKURA COMPOSITES”) and FUJIKURA COMPOSITES group companies.

This post has been prepared based on publicly available information, which we have not independently verified, and is not complete, timely, or comprehensive.

Although we believe that the information contained in this post is accurate and reliable, we make no representation or warranty as to the accuracy, completeness, or reliability of such information, or of any statements or oral communications regarding FUJIKURA COMPOSITES, FUJIKURA COMPOSITES group companies, or any other companies described herein. We also assume no responsibility for any such statements or communications, including any inaccuracies or omissions therein. With respect to public companies, there may be non-public information held by such companies or their insiders that has not been disclosed by those companies. Accordingly, all information contained in this post is presented “as is,” without any warranty of any kind, and we make no express or implied representation as to the accuracy, completeness, or timeliness of such information, or the results of its use. Readers should obtain their own professional advice and make their own assessment of the relevant matters. We disclaim any obligation or liability for any loss arising from, or in connection with, the use of all or any part of the information contained in this post, including any inaccuracies or omissions therein. Any investment involves significant risks, including the risk of a complete loss of capital. Any forecasts or estimates are provided solely for illustrative purposes and should not be regarded as indicating any upper limit of potential gains or losses. We may modify all or part of this post without notice to any person, but we are under no obligation to provide any revisions, updates, additional information or materials in relation to this post, or to correct any inaccuracies.

This post may contain content or quotations from, or hyperlinks to, publicly available third-party sources of information (“Third-Party Materials”). Permission to quote Third-Party Materials in this post may not have been sought or obtained. The contents of Third-Party Materials have not been independently verified by us and do not necessarily reflect our views. The authors and/or publishers of Third-Party Materials are independent from us and may hold views that differ from ours. The inclusion of Third-Party Materials in this post does not imply that we endorse or agree with any part of the content of such Third-Party Materials, nor does it imply that the authors or publishers of such Third-Party Materials endorse or agree with the views expressed by us in relation to the relevant matters. Third-Party Materials do not constitute all relevant news reports or views expressed by third parties regarding the matters discussed herein.

We do not intend, either by ourselves or through other shareholders, to propose at a general meeting of shareholders of FUJIKURA COMPOSITES that the business or assets of FUJIKURA COMPOSITES or FUJIKURA COMPOSITES group companies be transferred to a third party or discontinued. We also have no intention of engaging in any conduct whose purpose would be to make it difficult for FUJIKURA COMPOSITES or FUJIKURA COMPOSITES group companies to continue conducting their businesses in a stable and ongoing manner.

We currently beneficially own and/or have an economic interest in securities of FUJIKURA COMPOSITES and/or FUJIKURA COMPOSITES group companies, and may continue to beneficially own or have an economic interest in such securities in the future. With respect to our investment in FUJIKURA COMPOSITES and/or FUJIKURA COMPOSITES group companies, we may, on an ongoing basis and depending on various factors — including the financial condition and strategic direction of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, the results of discussions with FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, overall market conditions, other investment opportunities available to us, and the possibility of purchasing or selling securities of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies at prices at which we desire to transact — at any time, including through open-market or private transactions after we have established a position, buy, sell, cover, hedge, or otherwise change the form or substance of our investment, including securities of FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies, in any manner permitted by applicable laws and regulations, and we expressly disclaim any obligation to notify others of any such changes. We reserve the right to take any actions we deem appropriate in relation to our investment in FUJIKURA COMPOSITES and FUJIKURA COMPOSITES group companies. Such actions may include, but are not limited to, communications with the board of directors, management, or other investors.