On 11 May 2026, Hibiki Path Advisors SPC (hereinafter “Hibiki,” “we,” or “our”)’s core portfolio company Yagi Co., Ltd. (securities code: 7460, hereinafter the “Company” or “YAGI”) announced its new medium-term management plan “Medium-Term Management Plan 2029 (Business to Belief).” Leveraging its origins in textiles and the knowledge of materials and fashion trends accumulated through decades of global textile trading as fundamental sources of value, YAGI is now decisively shifting its focus toward pursuing growth on a new global stage as a brand-oriented enterprise through proactive investment. We are highly supportive of this plan, which is both meticulously designed and ambitious in scope. In our previous post, the first of a five-part series introducing YAGI, we focused primarily on the contents of this medium-term plan and introduced the “present and future” of YAGI. In this second post, we shall turn to the Company’s “past,” tracing its long history to explore how its corporate origins and core strengths were forged.

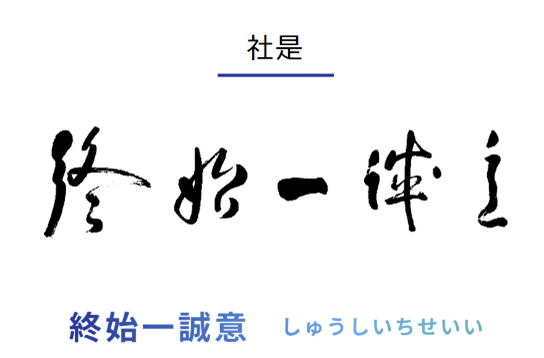

YAGI’s origin can be encapsulated in a single phrase previously introduced, which reflects the pure ethos of a traditional Japanese merchant and traces back to the Company’s founder, Mr. Yosaburo Yagi.

(YAGI Corporate Motto)

Sincerity from Start to Finish

(Source: YAGI website)

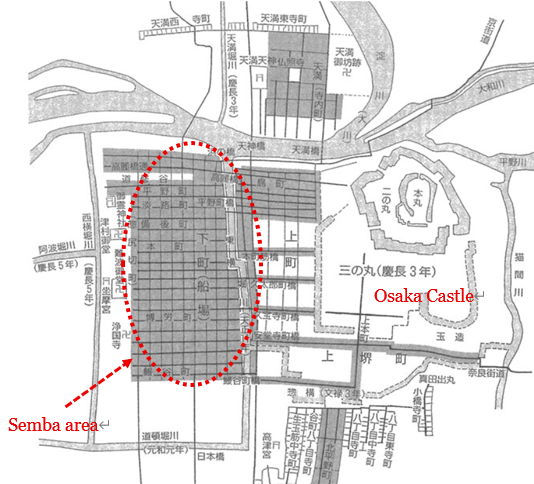

However, to properly understand the essence of the Company, it is first necessary to examine the broader arc of Japan’s textile industry and its rise and decline over decades. The story begins in Semba, Osaka, where YAGI is headquartered to this day. Semba emerged in the 1500s when Hideyoshi Toyotomi, a warlord, having achieved the first true unification of Japan, constructed Osaka Castle and gathered merchants from across the country to build a commercial district (see below for the old map of Semba).

(Osaka Castle and Semba in the Toyotomi era)

(Source: Hanabishi Co., Ltd. Website)

Located on flat land that served as prime sight for major battles during the Sengoku War period, the area evolved into a castle town and a national hub of commercial transactions. A network of moats and waterways, together with numerous landing stages for boats, is said to be the origin of the name “Semba (Using the character for boats for Sem)”. Mitsui Gofukuten (the origin of Current Mitsui group), which had expanded its business from Edo, opened a branch in Semba in 1691. In 1730, the first shogunate-approved rice futures exchange in Japan was established in Dojima. By the 1800s, the Omi merchants, residing in Shiga prefecture but who had developed its unique nationwide walk-trading routes, began to establish their bases in Semba to capitalize on its geographic advantages. It was in this central hub that Chubei Itoh, the founder of current both Itochu and Marubeni, opened his shop in 1872. Semba thus became a symbol of Japanese commerce.

In 1882 (Meiji 15), Osaka Spinning (now Toyobo Co., Ltd.), founded by Eiichi Shibusawa, commenced domestic production of spun yarn, achieving what had long been a national aspiration. This development triggered an explosive expansion in commercial activity related to the import and distribution of raw cotton, as well as the domestic distribution and export of cotton yarn and cotton products. In the midst of this textile-driven economic boom in Osaka, YAGI’s founder, Yosaburo Yagi, established “Yagi Shoten” in Semba in 1893 at the age of 28, embarking on his entrepreneurial journey. Having grown up in a family of rice trading business, he appears to have developed an innate sense for smart risk-taking. From this starting point, YAGI adopted “prudence first” and “sincerity from start to finish” as its core business ethics. These principles, encapsulated in the “sincerity and prudence” that have formed the Company’s DNA for more than 130 years, positioned YAGI to continue competing through successive waves of structural transformation in Japan’s industrial landscape.

At that time, large-scale capital was required to import raw cotton and export cotton yarn and cotton products from overseas. The major enterprises that focused on these segments achieved great success and came to be known as the “Kansai Cotton Five” companies, a lineage that continues today in large trading houses such as Itochu, Marubeni, and Sojitz. Other leading companies, including YAGI, which flexibly handled a broad range of cotton yarns and fabrics and grew by responding quickly to market needs, became known as the “Semba Eight.” A comparison with their present-day successors illustrates just how dramatic the tectonic shifts in Japan’s economic and social structure have been, and how intense the competition was (see below). Remarkably, YAGI is the only one among these companies that has retained its original founding name as its current corporate name.

(Source: Hibiki Path Advisors SPC compiled from Nikkei articles etc)

The fact that YAGI has survived as an independent company to the present day can be attributed, in our view, to two deeply embedded characteristics that actually sit further beneath the fundamental principles of “sincerity and prudence” its corporate DNA. Based on our interview and observation, we believe them to be “discernment and agility” and a “willingness to take calculated risk.” Below, we introduce several illustrative episodes that highlight these traits.

In more recent decades, YAGI’s overseas expansion from the 1990s and its downstream expansion into the apparel value chain can be seen as manifestations of these strengths. Trading businesses are constantly pressured over shrinking intermediary margins and the squeeze of value-add along the value chain. Broadly speaking, there are two typical strategies available. One is to expand horizontally into adjacent business domains. The other is to move upstream and downstream to deepen planning and proposal capabilities, thereby capturing a larger share of the value-added area within the value chain. A classic example of the former is Nagase & Co., Ltd., founded in 1832. Starting with starches, pastes, and dyes for the textile industry, Nagase later expanded laterally into chemicals in response to the rise of heavy chemical industries. Today, it handles electronic materials and biochemical products, continually reshaping itself like an amoeba in response to the times. YAGI, by contrast, has pursued the latter strategy of vertical expansion.

Rather than relying on simple commission-based trading, YAGI has built a flexible upstream network and strengthened its proposal capabilities. In the 1990s, the Company established sewing factories in China. As labor costs in China rose in the 2000s and “China plus one” strategies gained traction, YAGI rapidly shifted production to ASEAN countries such as Thailand and Laos. From the 2010s onward, the Company continued to reconfigure its production systems and procurement and logistics routes across Vietnam, Bangladesh, Myanmar, and other locations, thereby relentlessly pursuing a broad variety of materials and lower costs that are indispensable to enhancing its downstream proposal capabilities. At the same time, YAGI actively entered the downstream (brand and retail) domain to leverage these strengths. Beyond wholesaling to apparel companies, it has undertaken numerous M&A transactions and acquired overseas brand licenses since the 1990s, and has also experienced many setbacks and failures along the way. Amid these challenges, however, YAGI acquired TATRAS, now its core growth driver under the new medium-term management plan, in 2014. This acquisition can be seen as the product of YAGI’s “discernment and agility” in expanding upstream and its calculated “risk-taking” in entering downstream retail. The history and competitive landscape of the down jacket market, where TATRAS plays a leading role, and the outlook for this market will be discussed in great detail in the third post of this series so please stay tuned. Along this flexible M&A journey, in 2020, YAGI entered into a joint venture to operate NIKE stores in Japan (WINWIN YJV), another example of the Company’s fun initiatives. In its new medium-term plan, this business has been carved out as the newly defined “Retail” segment, in order to groom this retail management business to its new growth hub.

Nevertheless, to fully grasp YAGI’s true breed and how it survived the turbulent period from the high-growth era through the burst of the bubble, the Global Financial Crisis, and the Covid-19 pandemic, it is necessary to travel further back in time… Let us move back to the early 1900s. One notable episode from YAGI’s early years concerns its bold commitment to Kanegafuchi Spinning Co., Ltd. (“Kanebo”, now Kracie Holdings Ltd.), a leading player in the domestic spinning industry. Kanebo became highly regarded for supplying high-quality cotton yarn in large volumes on a stable basis, thereby driving the domestic production and upgrading of what had previously been a market dependent on imported yarn. It is not widely known, however, that YAGI’s founder, Yosaburo Yagi, played a pivotal role in this success.

In the early stages of development, Kanebo’s yarn was finer due to its delicate spinning method, which initially made the market skeptical due to its thinner look. Yosaburo Yagi turned this visual weakness into a strength by advising Kanebo’s top management, including then-president Sanji Muto, to emphasize in their narrative that the thinness of the yarn reflected the superior quality of the spinning process. This marketing pitch significantly boosted Kanebo’s reputation. Yagi Shoten benefited from increased trading business with Kanebo, laying a cornerstone for its early growth. During this period, the textile industry basked in its golden age, and by the 1910s textiles accounted for roughly half of Japan’s industrial production, with Osaka being mentioned as The Manchester of the East.

The next episode aroused during a tough post–World War II period. While Japan went through a massive industrialization phase back from the ashes, with huge capex going into heavy industries in manufacturing (Steel, petro-chemical, ships, automobiles etc), the relative importance of the textile sector declined. By the late 1960s, textile trading companies, including the Semba Eight Companies, entered a “winter” period marked by many bankruptcies and consolidations. Yet even in this challenging time, YAGI’s DNA “discernment and agility” are evident. In 1951, Toyo Rayon Co., Ltd. (now Toray Industries, Inc.), a flagship of the heavy chemical sector, began full-scale production of nylon, a new fiber derived from petroleum. At an early stage of market introduction, YAGI anticipated consumer needs and product characteristics and proposed various applications to Toyo Rayon, including nylon yarn for stockings and nylon for fire hoses. These proposals developed into sizable businesses. Embracing nylon—a material that posed a significant potential competitive threat to YAGI’s original cotton yarn business—as a core product required considerable courage. This ability to read structural change, combined with the willingness to take calculated risks, appears to lie at the heart of YAGI’s strengths.

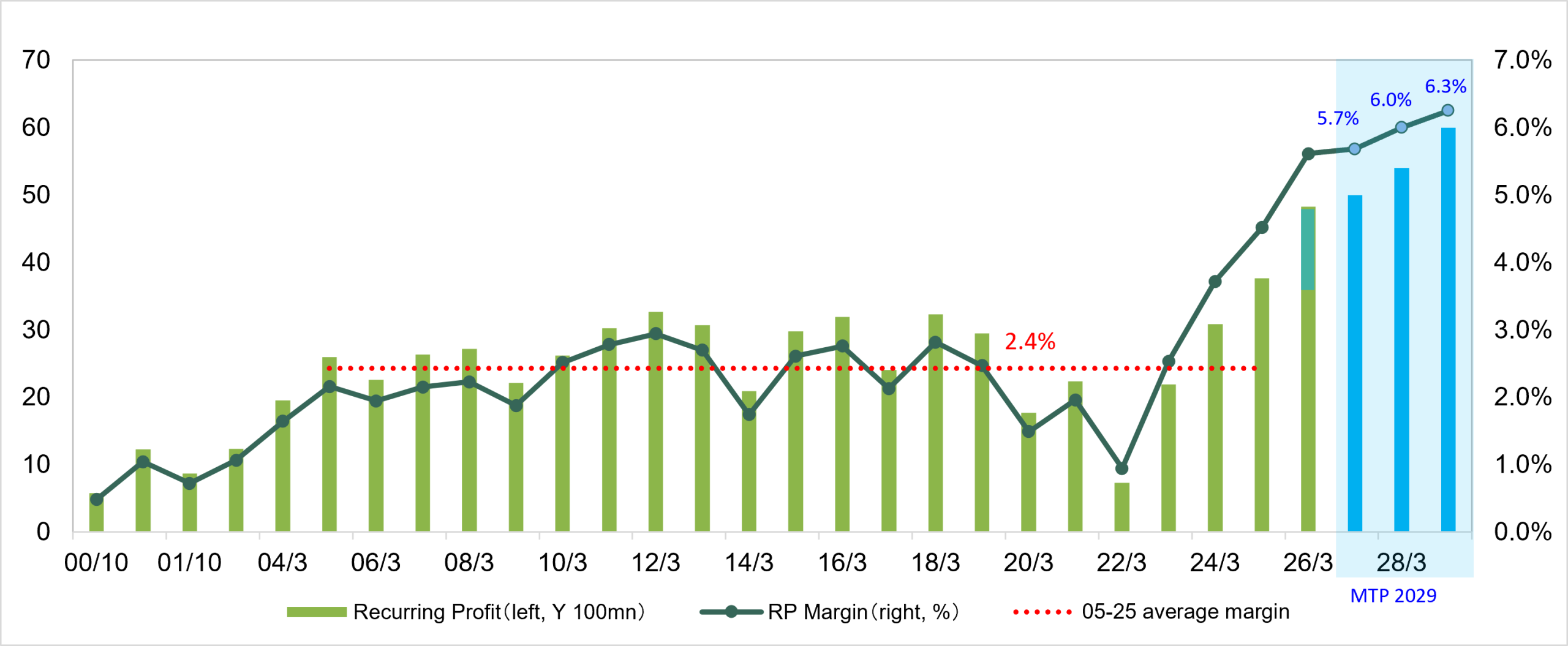

Today, Mr. Takao Yagi, its sixth president and, obviously a member of the founding family, serves in this role since 2016 leading its new growth strategy. In a 2017 interview with Nikkei, he described the Company’s defining characteristic as being “extremely nimble to always quickly adjust to changes like an amoeba.” It is precisely this characteristic that has enabled YAGI to survive the decline of the textile industry over 130 years, continue taking on challenges (taking calculated risks), and now climb to new heights under its latest medium-term management plan. As shown in the chart below, the Company now stands at an inflection point in terms of business transformation and leap in profitability. It has explicitly stated a medium-term target of achieving a ROE of 12%. Nevertheless, the current share price (4,405 yen as of May 28), which implies a price-to-book ratio of 0.77 times against actual BPS of 5,756 yen for the fiscal year ended March 2026, indicates that the market is still anchored to a legacy perception formed during a period of lower profitability as a simple trading shop. We actually discuss its medium-term plan and capital policy in great detail in our first post. We encourage those who have not yet read it to have a look since it will provide you with the flavor of YAGI’s (and Mr. Yagi’s) ambition towards the future.

(Source: Hibiki Path Advisors SPC compiled from Bloomberg and Yagi materials)

We are planning the third installment of this series in a few weeks. It will delve into the rich history and competitive dynamics of the down jacket market, TATRAS’s flagship product, and provide our perspective on the market’s future. We hope you will look forward to it!

P.S. – below is unfortunately only in Japanese but Yagi has just released its earnings and MTP explanation video this week. If you would like to have a look of how Yagi’s president speaks – please click and dive!

YAGI Press Release on MTP explanation video (25 May 2026)

(Screen capture from Yagi’s video)

(Reference)

14/May/2026 - Announcement of YAGI Co., Ltd. Medium-Term Management Plan 2029

This article does not constitute, and should not be construed as, an offer, solicitation, marketing, advertisement, inducement or representation in respect of any service or product. It does not provide any recommendation to buy or sell any investment product or any type of investment, to effect any transaction, or to refrain from any act, whether or not subject to conditions, nor does it express any opinion on the merits of any particular investment or investment strategy. Any examples of strategies or transactions are provided solely for illustrative purposes and do not represent past or future strategies or performance, nor do they indicate the likelihood of success of any particular strategy. This article does not constitute investment, financial, legal, tax or any other form of advice.

This article has been prepared based on publicly available information, which has not been independently verified, and is not intended to be complete, timely or comprehensive.

There is no intention, whether directly or through other shareholders, to make any proposal at the shareholders’ meeting of YAGI Co., Ltd. regarding the transfer to a third party or discontinuation of the businesses or assets of YAGI or any YAGI group company. Nor is there any intention to engage in conduct that would make it difficult for YAGI or any YAGI group company to continue conducting its business in a stable and sustainable manner.