Stock Compensation – Its Development in Japan

———————————————————————————————

Introduction

1. The Japanese Perspective on Board Compensation

2. 1990s – The Dawn of Officer Compensation as an Incentive

3. Officer Compensation as an Incentive – Penetration Period

4. Restricted Stock – the New Mainstream

5. Analysis on Current Situation – 50 Large Companies

6. Stock Performance

7. Institutional Investors’ Voting Guidelines

8. Why We Care So Much?

———————————————————————————————-

Introduction

The following article was published in The Nikkei last year right before June when many general shareholders’ meetings had taken place.

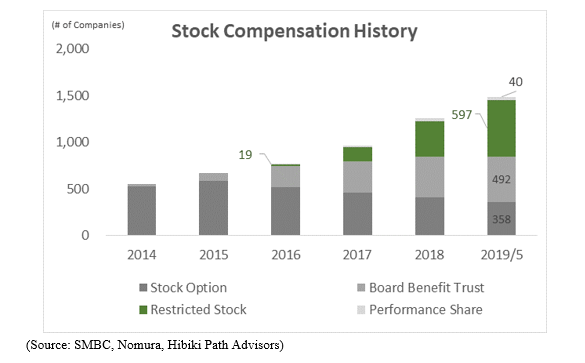

Amongst those, compensation via shares with restriction of transfer (Restricted Stock) emerged as a result of the 2016 tax reform and seems to be the most popular, with the actual number of companies introducing them in 3 years increasing to 597 (at end May 2019) as per below.

Its increased popularity was attributed to the longer duration until lifting of restrictions for sale as well as because of the favourable taxation, which enabled management to better reflect its desire to improve earnings and to align interest with shareholders.

In this white paper, we will be covering Restricted Stocks compensation, which has become the mainstream for officer remuneration, as well as its emergence, history and effects, in addition to being a substantial initiative in the future in terms of compensation governance. It is, in fact one of the most important consideration for us to review before deciding on investing to a company.

1. The Japanese Perspective on Board Compensation

In the globalized world of corporate governance, the general consensus for the logic behind the design of an officer compensation is to (1) recruit talented personnel (officers and board) into the company, (2) retain them, and (3) to provide motivation. “Motivation” here is to involve efforts that contribute to enhanced corporate value such as accelerated innovation/transformation, business restructuring, or M&As.

On the other hand, officer compensation under the old Commercial Code before the emergence of the stock option involved additions by way of merit, such as a retirement bonus and officer bonus as a form of compensation that included only small element of variable portion. This is considered to be related to Japanese practices of employment and advancement based on lifetime employment where the goal of career advancement for an employee was to become a board member, as well as the officer compensation system also being fundamentally regarded as an extension of the employee compensation system which does not involve much performance of the firm. Additionally, Japanese Corporate tax system was a large factor to prevent companies from implementing incentive pay scheme up to very recently. Let us first briefly go into the history of it.

2. 1990s – The Dawn of Officer Compensation as an Incentive

As Japan went through a painful depression after the bubble burst in the 1990s and due to increasing economic globalisation, there was finally a growing voice to lift the ban on stock options that had gained popularity as a means of compensation in the U.S.

Stock options were then introduced to Japanese corporations as a result of the emergence of the stock warrants method in the mid-90s and the revision to the Commercial Code in 1997, although the latter was limited to existing employees and granted free of charge – i.e. it was regarded as a “gift” to the recipients from companies. While it opened up the path to incentive pay and acted as a big stepping stone for the future, it was far from tax efficient for the issuer (company) as it was denied by the tax authority as tax deductible expense for companies.

In 2001, deregulation removed the restrictions on the recipients of the grant including the limitation on exercise periods and the amount of grants. This paved the way for more companies to consider and issue stock options to the board/senior officers, and employees. However, the biggest hurdle was on the companies’ disability in designing a flexible compensation scheme due to constraints in the tax system. Board incentive compensation with stock options remained at an extremely low level as National Tax Agency made it so difficult for the recipients to defer tax when they exercise the options. As most of the options are not designed as tax deferrable, a Tax invoice was issued immediately after the exercise of the stock options resulting in the recipients being forced to sell the stocks received from the option in order to fund the tax payment.

Still, many companies tried to use such option scheme and there became a trend to grant stock options with 1yen exercise price (so essentially giving full value of a stock to the officers) – which is a quasi-stock compensation. Following that trend, in 2005, a big change was introduced in the Companies Act in 2005. Rather than being considered as a “thank you gift”, “Board Bonus” was categorised for the first time in Japan’s corporate history as part of management compensation, and tax reform followed such change in 2006. Technically speaking, this 1 yen option became tax deductible expense for the companies (under some restrictions), and board member recipients were allowed to receive special tax treatment when it was exercised at the time of retirement. This was revolutionary (at least in Japan context).

Based on such changes, companies started using this 1 yen stock option as a replacement for the “fixed” retirement bonus scheme, urging senior members to exercise at their retirement. It did, at least, make sense from the interest alignment stand point with shareholders, so the abolishment of the retirement bonus scheme and the introduction of the 1 yen stock option became one of the trends in management/officer compensation dynamics up to 2015.

3. Officer Compensation as an Incentive – Penetration Period

In 2015 “Study Group for Effective Corporate Governance Systems”, a quasi-government working group, started its discussion to allow and introduce more flexible incentive scheme for corporate officers and board members, alongside newly introduced Corporate Governance (“CG”) code (in June 2015). As a result of the discussion, CG was revised in June 2018: ‘board remuneration should include incentives on mid-to-long-term business and risks associated with it, in order to groom healthy entrepreneur mindset’. Additionally, in the same Supplementary, it mentioned that ‘the board should design management renumeration systems such that they operate as a healthy incentive to generate sustainable growth, and determine actual remuneration amounts appropriately through objective and transparent procedures’. Last but not least, the statement ‘the proportion of management remuneration linked to mid-to-long term results and the balance (remuneration) of cash and stock should be set appropriately’ framed how companies should introduce compensation structures. As a result, companies were suddenly forced to start thinking hard on stock compensation and “the connection of that with mid-and-long-term business results”.

While it took such a long time to reach this level since 1990s, in part (or most) due to rigid tax regulation, it is also a truth (maybe to your surprise) that such mentality has always been in place for many Japanese companies. It was mentioned by one of the most famous CEO in Japan’s Corporate history Mr. Akio Morita, the founder of SONY, nearly 60 years ago. He mentioned in a magazine interview in 1964, “the first thing Japanese companies need to tackle is the complete redesign of the fundamental thoughts about organizational and individual work aspect in a company.” And even added that “the notion of lifetime employment amongst the employees is so dangerous that it gives the people incentive to stand-still and live a stable life rather than take risks to do something to grow the company”. It was likely not easy to deny the traditional system back then in public, and it was his small warning towards the stable and fixed arrangement for employment contract and salary design.

4. Restricted Stock – the New Mainstream

We have been discussing the unique history and evolution of Japan’s director/officer incentive compensation scheme. Now, let us look at the more recent changes in tax system and how it finally brought various new types of share compensation.

In 2016, two major revisions were introduced in relation to board/officer compensation as per below.

(1) Restricted stock compensation became tax deductible for corporates

(2) Restricted stock, if exercised at the time of retirement, becomes retirement compensation

for the board members and senior officers

It may be striking to some of you that these revisions were only put in place recently. Prior to 2016, if a company has transferred stocks to some of its valued lieutenants as part of compensation, it was not regarded as expense, and the value was completely taxed by the government as opposed to tax deductible 1yen stock options (so nobody used Restricted Stocks). Additionally, people had to pay income tax for value of the stock compensation received immediately in the same year even if they cannot sell it for many years as part of restriction – it is a complete deal killer from both sides. The lack of incentive-based compensation was caused more by tax considerations rather than the ambiguous ‘Japan culture’ problem which many people wrongly assume. Companies and officers behaved rationally for not considering any Restricted Stock compensation because of the tax consequence for themselves and the recipients.

There are a several forms of share-based compensations available in Japan now (as shown in the following table), but we, as an investor thinking about this for many years, prefer this “Restricted Stock (RS)” compensation as it finally became tax efficient after 2016.

Compensation through RS has superiority over others on three fronts; (1) both retention and incentive, (2) alignment of interest with shareholders, and (3) low cost of managing the program by companies. While there are more innovative means such as “performance share units” evolving to become a mainstream measure especially in the US, we feel it is too early for most Japanese companies as it requires a well governed design which defines and measures the “performance” of each of recipients (i.e. board members), a heavy burden to both develop and maintain fairly.

5. Analysis on Current Situation – 50 Large Companies

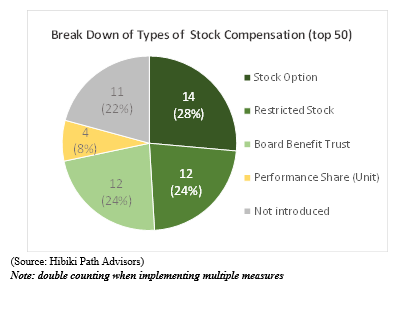

Let us look now into the real data of how stock compensation is currently being used by companies. We would like to take a closer look at top 50 market cap companies listed in the Tokyo Stock Exchange. It is positive that the majority of companies (39 companies) have already introduced some form of stock compensations.

Due to the wobbly history of tax arrangement to these incentive schemes (as we have discussed), even now, we can see that 1 yen stock option is the most popular incentive scheme used by 14 companies (it is the remains of prior efforts by companies), followed by 12 companies tied in numbers between Restricted Stocks and Board Benefit Trust respectively (see below pie chart), a newer introduced measures.

It is interesting to see “Board Benefit Trust” also being popular amongst large companies and we suspect the reason to be: (1) it has tax merit to company since 2016 tax reform and (2) for larger companies, a pool of incentive recipients is large enough to pay costs for establishing and running the trust (running cost, mostly paid to the custody trust-banks, are high); and (3) relative flexibility of incentive scheme design.

However, things are moving fast towards Restricted Stocks. In the past 3 years, five companies abolished the Stock Option scheme, of whom four replaced it with Restricted Stocks and only one company shifted to Board Benefit Trust.

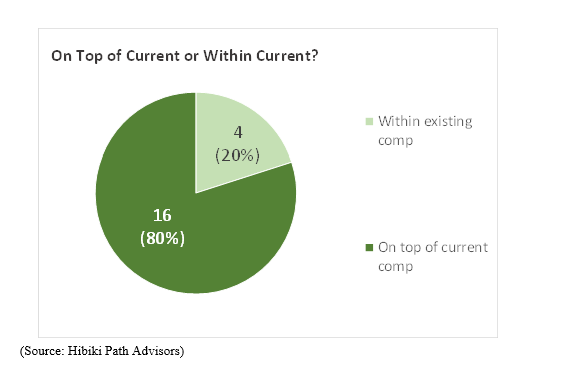

In practice, the biggest reason for such increase in penetration of Restricted Stocks is that this incentive scheme requires virtually no operational costs and, secondary, the recipient is not required to cash out to fund the tax for receiving such a stock arrangement (which was an ill-conceived, but actual, tax regulation that had been in place for all these decades) – very simple remedies. Ministry of Economy, Trade and Industry (“METI”) also encourages stock-based compensation to be added on top of existing compensation in its handbook, citing that it would be ideal to obtain shareholder consent for additional compensation by an AGM vote. With that endorsement from the government, 80% of Restricted Stocks are set in addition to the existing cash compensation framework and it indicates the intended nature for this compensation is considered as incentive based compensation for the board.

This data implies that (1) historically Japanese board compensations were low in value and low in incentives, (2) corporates and market are both starting to accept that such incentive measures are “necessary”; and (3) it is good for corporate governance to have increased alignment of interest between the management team and shareholders.

Regarding the restricted (vesting) period, the majority of companies (11 companies) have a restriction period of 3 years from shares granted, followed by a group of companies with an extreme long term of 30 years (6 companies). Major international proxy-advisors as well as Japanese leading institutional investors mention that they will vote against the plan if vesting is permitted within 3 years and the share grant is not conditional on an earnings hurdle I.e. market participant views are in-line with the METI’s guideline. We are positively surprised to know that more than 10% of the top 50 market cap companies have 30 years (!) vesting periods on their stock grants. It is, naturally, designed to be of real value only when the board and senior officers are retiring. These six such companies are listed below.

One setback here is the fact that there are only 4 companies with performance-linked restrictions (n.b. performance includes financial results and stock price), features which better aligns with shareholder interests.

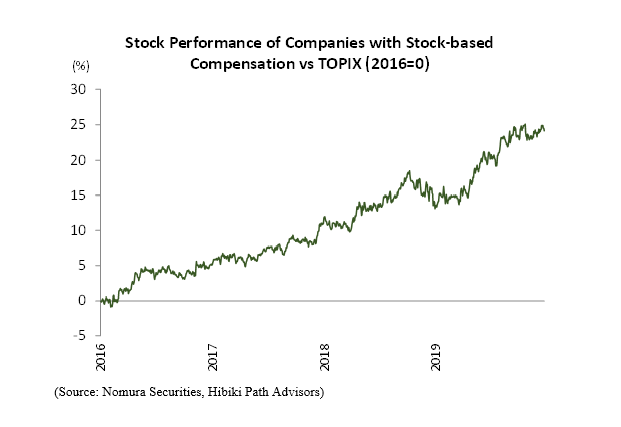

6. Stock Performance

When board compensation is well designed and functions properly as incentive scheme, it will mitigate inefficiencies caused by Agency Problems and leads to creation of long-term corporate value and market tends to react quickly to such change sooner rather than later. We will examine this hypothesis here.

The graph below is a simple average of stock price for the top 20 market cap companies that have stock compensation already in place, in relative to Topix. It is striking to know that since 2016, the group has constantly outperformed Topix every year up to now, and cumulative relative outperformance is 25% in four years.

We believe that there are two factors working behind this surprisingly strong result. One of the factors is the market sentiment. Investors view increased stock compensation as a message of increased confidence within the management team. The second factor is the complete flip-side of what the market considers, but it can be said that those companies who plan to implement such stock compensation measures generally have a share price more “sensitive” to improving corporate governance. These company managements typically have more confidence towards their future values. Conversely, if the company management has no confidence over its value creation toward the future, they would rather receive everything in cash and continue to hit-the-can as it makes all good sense.

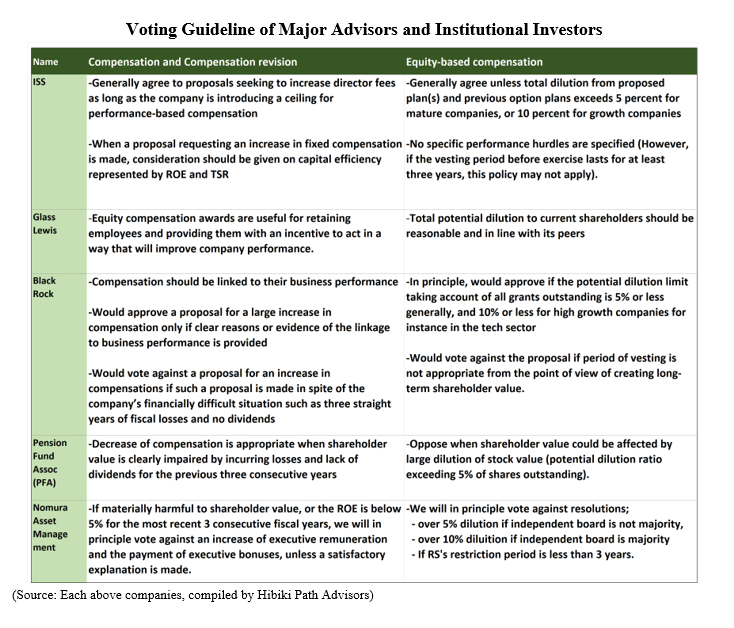

7. Institutional Investors’ Voting Guidelines

Lastly, before we move on to our conclusion, we would like to turn to investors’ point of view for a short while. Apparently, major international proxy-advisors and Japanese leading institutional investors both welcomes board/officer incentives linked to company’s performance (please see table below).

As mentioned below in their guidelines they generally would agree as long as (1) new stock issue would not cause either 5% or 10% (depending on different circumstances) dilution, and (2) vesting period not less than 3 years when no earnings target clause is present.

We view this as modest and agreeable guidelines and as such we have also made a shareholder proposal to Sanyo Shokai (8011) in 2019 to introduce stock compensation to board and officers with 3 years vesting period (because of our proposal, company came out with similar proposal and has been approved in the AGM in March 2019).

8. Why We Care So Much?

In our stock compensation presentation for companies we invest in, we introduce two key phrases from Procter and Gamble (P&G)’s long standing “Core Values” and “Principles”, as per below.

P&G is, no doubt, a prominent global business but with also a very high reputation from its own employees (and retirees) in terms of great work environment, human ethics and compensation package, of course, with solid stock purchase plan for most of its long-term employees. While excellence of business derives from so many different factors, P&G has kept its strong culture since it was established 183 years ago and there are many things we can learn from such principles. It is impressive to see that those principles are taking the ownership mentality extremely seriously as much as quest for quality and customer care. We are duly impressed with the fundamental message it sends out both to employees, and to shareholders. In our effort towards companies, we are only trying to remind such virtue to management teams in Japan.

Japan had gone through an extremely unique and different corporate history until very recently compared to those in Western countries with long capitalism tradition. A few decades of phenomenal growth after WWII also reinforced a peculiar corporate system that put “harmony”, “long-term commitment” and “sacrifice” first and foremost (even before profits) and it has resulted in a linear compensation scheme with contempt towards “pay-for-performance” type mindset. Tax system also reinforced such thinking through hostility towards incentive-based bonus arrangements.

Starting with 2005, and definitely after 2016, we have, finally, just entered a stage where companies and those management teams are starting to think seriously about the correct incentive scheme to compensate for those senior officers and boards whose contribution is vital in value creation. Prior to 2005, sadly, companies were essentially “handcuffed” when trying to reward those lieutenants properly, and so companies, based on their own rationale, invented titles such as “senior advisors (Soudan-yaku)” to reward those senior management whose contribution were monumental until long after their retirement – providing them with cars, private-room in the office, advisory fees etc.

As you can see, tax rules change suddenly, but companies adjust gradually over time. We are now seeing fundamental land-slide shift in adoption of share-based incentive measures, and while the direct impact is not easy to measure, we are encouraged to see more and more dynamic corporate strategies such as group reorganizations, TOBs, and M&As in general happening in the market place. Many different factors are contributing to increased dynamism in the market but we have a strong view that penetration of stock compensation is one extremely powerful basso-continuo for the phenomenon.

We would like each and every senior member (board members and the officers, managers) in our investee companies to think and act like owners and we continue to push for further increase in such compensation measures to them which will, over-time, bring them opportunity to become financially rewarded by the time they start thinking about retirement, in addition to being thanked by their shareholders. Corporate success, individual (board/senior member) happiness, and shareholder value creation can, and should, be considered as one same goal to be achieved by all the stakeholders and it is something we consider as a vital factor behind successful long-term investing.

(29 January 2020)

Shinji Tanioka, Senior Analyst

Yuya Shimizu, Chief Investment Officer

Hibiki Path Advisors Pte. Ltd.